Listen up. Buying a short sale home in Los Angeles isn’t your typical Sunday open house stroll. It’s a whole different beast—a strategic play to snag a property for less than what the owner owes the bank. The catch? The lender has to sign off on the deal, and that’s where the real game begins.

While the process can feel like running a marathon in flip-flops compared to a traditional purchase, it’s a killer move to lock down a property at or below market value, especially in a city as notoriously cutthroat as LA.

Why Short Sales Are LA’s Hidden Opportunity

When you hear “short sale,” your mind probably jumps back to the 2008 financial crisis. Let’s get one thing straight: the short sale market in Los Angeles today is a completely different animal. This isn’t about a massive economic meltdown; it’s a more subtle, ongoing market correction happening one property at a time.

This quiet wave of opportunities is bubbling up for a couple of key reasons. The end of pandemic-era mortgage forbearance programs has left some homeowners facing a financial reality they can no longer put off. Couple that with the insane cost of living in LA, and you’ve got the perfect recipe for distressed properties that most buyers are completely overlooking.

The Real Reasons Homeowners Are Selling Short

What’s really fueling this hidden market are the financial curveballs that catch homeowners totally off guard. Many are just now discovering unexpected second liens or ticking time-bomb balloon payments that were buried deep in their loan documents from years ago.

We’re also seeing a lot more situations involving reverse mortgages where the heirs can’t afford to pay off the loan balance, forcing them to sell the property.

These scenarios create highly motivated sellers and banks that are actually willing to play ball. A lender would almost always prefer a short sale over the soul-crushing, expensive process of foreclosure. Foreclosure means lawyer fees, property maintenance, and the very real risk of the house falling apart while it sits empty. A short sale, on the other hand, keeps the property occupied and gives the bank a much faster, cleaner exit.

A short sale isn’t some desperate fire sale; it’s a cold, hard business decision for the lender. Their goal is to cut their losses, and a solid offer from a qualified buyer is often the best way to do that.

A Growing Trend Beyond LA

This isn’t just an LA thing; it’s a pattern we’re seeing pop up nationwide. In the last few years, short sales have gotten a second look in major U.S. markets, all thanks to economic pressures like rising consumer debt and the fallout from pandemic loan forbearance.

Markets like Sacramento, Phoenix, and parts of Florida have seen a shocking 25% to 140% jump in short sale deals, year-over-year. This surge is happening because so many homeowners are uncovering those hidden second liens or balloon payments years after they hit pause on their mortgage during COVID-19. You can dive deeper into these trends and see how savvy investors are jumping on these distressed properties.

Knowing the difference between a short sale and other distressed property types is crucial. Before you dive in, you need to understand exactly what you’re getting into. We’ll break down the key differences below. For more context, you can also check out our guide on how to buy foreclosure properties to see how these two investment strategies stack up. This knowledge isn’t just academic—it’s your inside track to an undervalued market niche, giving you the context to spot these opportunities before everyone else does.

Short Sale vs Traditional Home Purchase

So, what are you really signing up for with a short sale? It’s not your typical LA home purchase, that’s for sure. Here’s a quick breakdown of what to expect.

| Factor | Short Sale Purchase | Traditional Purchase |

|---|---|---|

| Timeline | Highly unpredictable; 3-12+ months is common. | Predictable; typically 30-45 days. |

| Price | Often below market value, but the final price is up to the lender. | Set by the seller, negotiated with the buyer. |

| Approval | Requires approval from the seller’s lender(s), which can be complex. | Only requires agreement between buyer and seller. |

| Condition | Almost always sold “as-is”; often in need of repairs. | Varies, but buyers can often negotiate repairs. |

| Competition | Less competition from typical buyers due to complexity and timeline. | High competition, especially for desirable properties. |

The takeaway is simple: short sales trade speed and certainty for a potential discount. If you have the patience and the right team, it can be a fantastic way to get a deal. But if you need to move quickly, a traditional purchase is the safer bet.

How to Find and Qualify LA Short Sale Deals

Finding a legitimate short sale gem in Los Angeles isn’t about luck. It’s about knowing where to look when everyone else is staring at the same screen. If your only move is scrolling through the MLS, you’re already late to the party. The best deals are often locked up long before they hit the open market, which means you need a proactive, almost guerrilla-style approach to find them.

This is where the real work—and the real opportunity—begins. Forget passively waiting for listings to appear. It’s time to build a deal pipeline that’s actually worth your energy and your money.

Building Your Deal-Finding Machine

First things first: ditch the lone wolf mentality. You need a team, and your most valuable player is a battle-tested real estate agent who specializes in distressed properties. I’m not talking about the agent selling luxury condos in Beverly Hills. You need someone who lives and breathes the gritty world of short sales and foreclosures.

A great agent has a network. They know the attorneys, the title officers, and even some of the bank contacts. They hear about homeowners heading toward default long before a “For Sale” sign ever hits the lawn. That inside track is your single biggest advantage in a market as cutthroat as LA.

Beyond your agent, it’s time to get your hands dirty with some old-school detective work.

- Public Records Deep Dive: The LA County Registrar-Recorder/County Clerk’s office is a goldmine. You can search for Notices of Default (NODs), which are public filings signaling a homeowner is behind on their mortgage. This is the starting gun for a potential short sale.

- Driving for Dollars: It sounds old-fashioned, but it works. Drive through neighborhoods you’re targeting and look for visible signs of neglect—overgrown lawns, piled-up mail, or obvious deferred maintenance. These are often the first clues that a homeowner is under serious financial strain.

- Targeted Networking: Connect with local real estate investor associations (REIAs). These groups are crawling with wholesalers, flippers, and other investors who might have off-market short sale leads they can’t take on themselves.

The goal isn’t just to find listings; it’s to find problems you can solve. A homeowner facing foreclosure has a massive problem, and a well-structured short sale offer can be the perfect solution for both them and the bank.

Vetting the Deal Before You Dive In

Finding a potential short sale is just the first step. Now comes the most critical part: qualifying the deal to make sure it’s not a money pit in disguise. Wasting months on a deal that was dead on arrival is the ultimate rookie mistake, and I’ve seen it happen too many times.

Your initial due diligence has to be fast and ruthless. Your very first move should be to run a preliminary title search. You absolutely need to know who has a claim to that property. A single mortgage is pretty straightforward, but many distressed properties have a tangled mess of liens.

Common Liens to Watch Out For:

- Second or Third Mortgages: These junior lienholders have to approve the short sale too, which adds another layer of negotiation and another chance for the whole thing to fall apart.

- IRS or State Tax Liens: The government always gets paid first. These liens can be notoriously difficult and time-consuming to negotiate down.

- Mechanic’s Liens: A contractor who wasn’t paid can slap a lien on the property, creating yet another creditor you’ll have to satisfy.

Once the title picture is clear, it’s all about the numbers. You need to quickly estimate the After-Repair Value (ARV)—what the home will actually be worth after you fix it up. A quick walk-through with a trusted contractor can give you a ballpark figure for the rehab budget.

If the numbers don’t work on paper, walk away. Don’t let emotion or “what if” scenarios cloud your judgment. This vetting process is your filter, making sure you only pursue buying short sale homes that have a real shot at being profitable.

Decoding the Short Sale Approval Gauntlet

You found a diamond in the rough. You qualified the deal. Now comes the part where most buyers give up: the approval gauntlet. Let’s be real—this isn’t a simple chat with the homeowner. This is a bureaucratic marathon with their lender, a massive financial institution that moves at the speed of smell.

This is where deals are made or, more often, die a slow, painful death from lost paperwork and soul-crushing silence. Your secret weapon is understanding the bank’s playbook. Knowing what they want, why they want it, and how to hand it to them on a silver platter is what separates a successful investor from a frustrated ex-buyer.

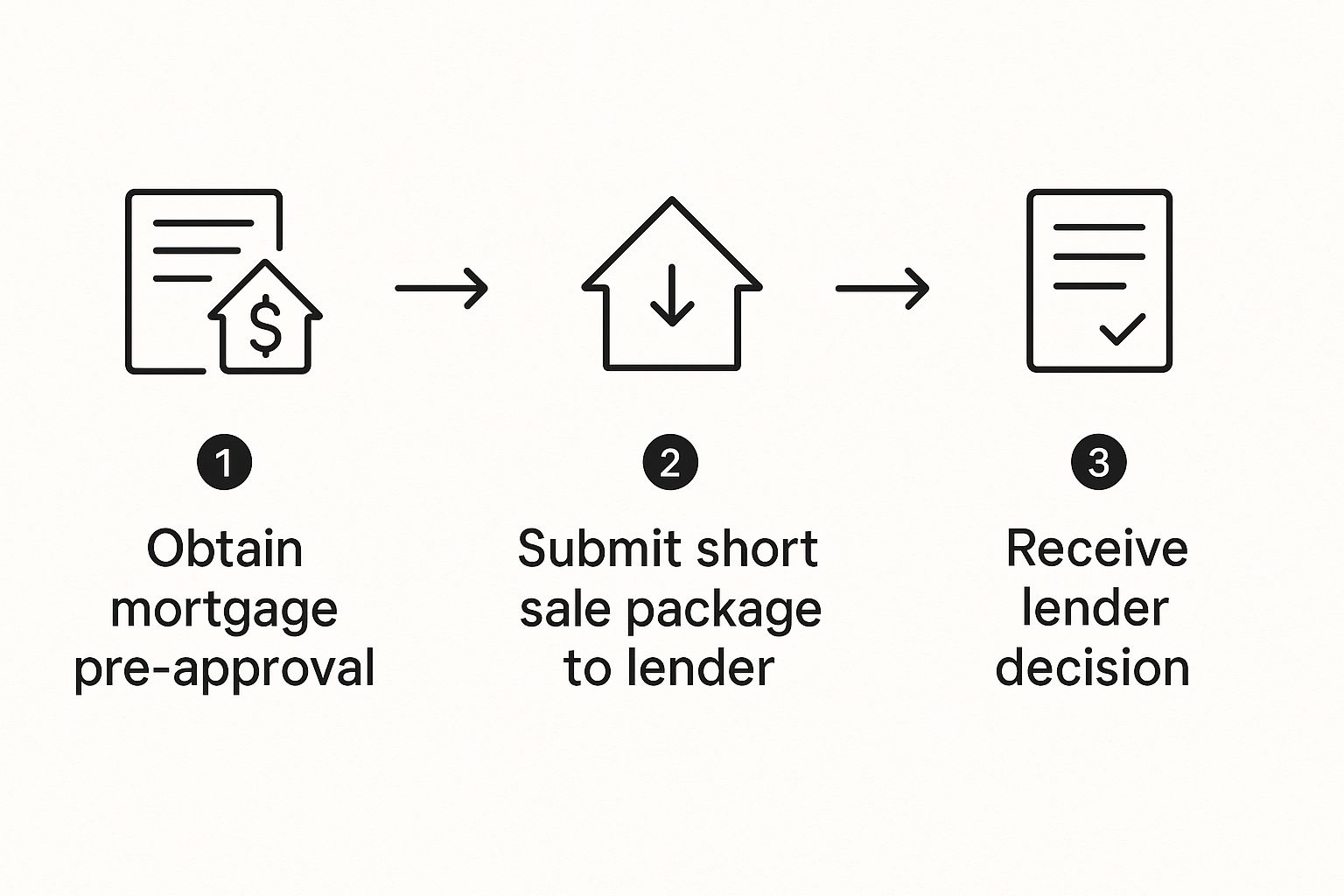

The infographic below lays out the high-level journey your offer takes once the lender gets involved.

It maps out the core steps from getting your finances straight to the bank’s final verdict, shining a light on that critical submission phase.

The All-Important Short Sale Package

Think of the short sale package as your formal application to the bank. A sloppy, incomplete submission is the fastest way to get your offer chucked into a black hole. The bank needs a complete story explaining why they should take a loss on this loan, and it’s your agent’s job to tell that story perfectly.

A rock-solid package absolutely must include:

- Your Offer: A clean, concise purchase agreement with your number.

- Proof of Funds: Whether it’s cash in the bank or a pre-approval letter, they need to see you can actually close this thing.

- The Seller’s Hardship Letter: A detailed, compelling narrative from the homeowner explaining exactly why they can’t make the payments anymore.

- Financial Documentation: The proof. This means the seller’s bank statements, tax returns, and pay stubs to back up their story.

- A Preliminary Settlement Statement: An estimate of all closing costs, showing the bank precisely what their net proceeds will be.

Your offer isn’t just a number; it’s a business proposal to the bank. A clean, complete package tells them you’re a serious, professional buyer who isn’t here to waste their time.

Surviving the Waiting Game

Once the package is in, the real test begins. The complexities of short sales are infamous in real estate, often because the lender’s own house is a mess. I’ve seen countless agents get frustrated because the bank’s servicing departments are understaffed and clueless about these deals. It’s a mountain of paperwork, and their backlogs create massive delays. This is why so many traditional buyers bail. For more on these challenges, the National Association of REALTORS® offers some great insights.

Your file gets assigned to a loss mitigator at the bank, but that person is probably juggling hundreds of other files. Don’t expect daily updates. Weeks can crawl by with absolute radio silence. It’s maddening, but it’s normal.

During this period, the bank will order its own valuation, usually a Broker Price Opinion (BPO). This isn’t a full appraisal; it’s a quick assessment by a local agent to peg the property’s current market value. Your offer has to be in the same ballpark as this BPO for the bank to even take you seriously.

Understanding the Bank’s Motivation

Here’s the single most important thing to remember: the bank doesn’t care about the seller’s feelings or your investment dreams. They care about one thing and one thing only: minimizing their financial loss. Their entire decision is a cold, hard calculation comparing your offer to the alternative.

- Your Offer: The purchase price minus closing costs, commissions, and any unpaid property taxes or liens. This is their certain, immediate outcome.

- Foreclosure Alternative: The estimated auction price minus lengthy legal fees, property upkeep, and the risk of the home falling apart while it sits vacant. This is their risky, delayed outcome.

Your offer needs to be the clear financial winner. It has to be just sweet enough to convince the bank that taking a small, certain loss now is way better than risking a bigger, uncertain loss down the road. Adopt that mindset, and you’ll get your deal across the finish line while everyone else is still waiting for the phone to ring.

Crafting a Winning Offer the Bank Will Approve

Making an offer on a short sale isn’t about lobbing a lowball number at the wall to see what sticks. That’s the fastest way to get your offer tossed in the trash. But if you come in too high, you’ve just negotiated against yourself and erased the entire reason you were targeting a short sale in the first place.

This is a strategic game. Your opponent isn’t the homeowner—it’s their lender. The goal is to put together an offer so clean, logical, and financially sound that the bank’s loss mitigator sees it as their easiest path out. You have to convince them that approving your deal is a much smarter business decision than letting the property sink into the black hole of foreclosure.

Justify Your Price with Hyper-Local Data

The bank’s decision pivots on a single document you’ll never get to see: their Broker Price Opinion (BPO). This is their own internal valuation, and if your offer isn’t even in the same ballpark, it’s dead on arrival.

Forget Zillow. You need to back up your offer with cold, hard, hyper-local comparable sales (comps).

Your agent needs to pull comps for similar properties sold within the last 90 days in that specific LA neighborhood—not just the zip code. We’re talking blocks, not miles. Ideally, these comps should include other distressed sales, like REOs or even other short sales, because they paint a much more realistic picture of value.

Presenting these comps with your offer accomplishes two critical things:

- It shows you’ve done your homework. You aren’t just pulling a number out of thin air; it’s grounded in real market data.

- It builds your case. You’re preemptively arguing against a potentially inflated BPO, giving the bank’s asset manager the ammunition they need to justify your price to their higher-ups.

Your offer isn’t just a number; it’s a narrative. The story you’re telling the bank is, “This is the true market value of this ‘as-is’ property right now, and my offer reflects that reality.”

The Power of a Clean Offer

In the world of short sales, simplicity is everything. Lenders are buried under complex files and messy paperwork. An offer that’s clean, with minimal contingencies, stands out like a beacon of hope. Every contingency you add is another hurdle, another potential delay, and another reason for the bank to pick someone else.

You should never waive your inspection contingency, but other demands can absolutely kill your deal. Asking for seller credits to cover closing costs? That’s usually a non-starter. The bank is already taking a loss; they have zero interest in sweetening the pot for you.

Remember, their entire focus is on maximizing their net proceeds. An offer for $450,000 with no strings attached is often far more attractive than an offer for $460,000 that asks for $10,000 in closing cost assistance.

A strong proof of funds or a rock-solid pre-approval letter from a reputable lender is non-negotiable. It proves you’re a serious, qualified buyer who can close quickly the moment they finally give you the green light.

Navigating the Inevitable Counteroffer

Don’t be surprised or offended when the bank counters your offer. It’s a standard move in their playbook. They are legally obligated to try and get the best possible price for their investors. This is exactly where all your prep work pays off.

Analyze their counter. Is it close to your number, or is it absurdly high? If it’s the latter, they’re likely basing their price on an unrealistic BPO. This is your chance to push back—politely but firmly.

Have your agent resubmit your best comps, maybe adding photos that highlight the property’s poor condition, to argue why their number is out of line with the property’s “as-is” reality. For a deeper dive into these tactics, our guide on how to negotiate a home price provides a great framework.

Ultimately, your offer is a compelling business case. You’re showing them that you are their quickest, most reliable path to cutting their losses. Make it easy for them to say yes.

Financing Your Deal and Getting to the Finish Line

You’ve navigated the maze of paperwork, put together a killer offer, and finally got the bank’s attention. So now what? It’s time to line up the money and actually close this thing.

But first, forget everything you know about a standard 30-day mortgage process. Financing a short sale requires a totally different mindset, one that’s built for painfully long timelines and properties sold “as-is,” warts and all.

This final stretch is where deals often fall apart. Financing hiccups and closing-day surprises can kill a transaction that took months to build. Staying on top of every detail is the only way you’re getting those keys.

Choosing the Right Financial Weapon

Your financing choice can make or break a short sale deal. The lender wants one thing above all: certainty. A slow, complicated loan approval process introduces risk, and banks hate risk. While a conventional loan is technically possible, it’s usually the wrong tool for this specific job.

Short sale properties are always sold “as-is,” which means they often have deferred maintenance issues that wouldn’t pass the strict appraisal requirements for government-backed FHA or VA loans. This is exactly why seasoned investors lean on more flexible, investor-friendly options.

- Cash Is King: An all-cash offer is the ultimate power move. It completely removes financing contingencies and appraisal headaches, making your offer incredibly attractive to a loss-averse lender.

- Hard Money Loans: These are short-term, asset-based loans from private investors. They close fast and focus on the property’s value, not your personal income, which makes them perfect for homes needing repairs.

- Private Capital: Similar to hard money, this means borrowing from an individual or a small group you know. If you have a strong network and a solid deal, you can often negotiate more flexible terms.

The bottom line is this: your financing needs to be as patient as you are. A pre-approval letter for a conventional loan might expire long before the short sale lender ever gives you a final decision. Make sure your lender understands the unpredictable timeline.

Dissecting the Short Sale Approval Letter

After months of radio silence, it finally arrives: the short sale approval letter. This document is your green light, but it’s not just a simple “yes.” It’s a legally binding agreement packed with critical details, deadlines, and potential landmines.

Read every single line. This letter dictates the exact terms of the sale, and you need to look for specific clauses. Pay extremely close attention to the closing deadline. Banks are notoriously rigid on this; if the letter says you have 30 days to close, you have exactly 30 days. Missing this deadline could torch the entire deal.

Also, look for any language about deficiency judgments. The letter should clearly state that the lender is waiving their right to pursue the seller for the remaining debt. This is what protects the seller and ensures a clean break for everyone.

The Final Push to Closing

With the approval letter in hand, the race to the finish line begins. This is where your agent and title company need to work in lockstep, coordinating all the moving parts of a notoriously unpredictable process.

While you’re focused on your deal, remember the bigger picture. Macroeconomic factors like rising debt costs have increased the number of distressed listings, making short sales a key play for sharp investors. If you want to dive deeper, you can explore the latest trends in global real estate investment on ubs.com.

Your final steps before getting the keys include:

- Scheduling the Final Walkthrough: This is non-negotiable. You have to verify that the property’s condition hasn’t changed since your first visit. Check for new damage, removed fixtures, or signs of vandalism—it happens.

- Reviewing the Closing Disclosure (CD): Your lender will send this document at least three days before closing. Compare it meticulously against your initial loan estimate to make sure there are no surprise fees tacked on at the last minute.

- Coordinating with the Title Company: Ensure all parties—you, your agent, the seller’s agent, and the lender’s reps—are scheduled and ready for the closing appointment.

Getting pre-approved for your mortgage is a crucial first step that shows you’re a serious buyer and helps streamline the entire process. For more detailed guidance, check out our guide on how to get pre-approved for a mortgage. Staying organized and communicating relentlessly with your team is the key to successfully navigating the final, often chaotic, steps of buying a short sale home.

Your Questions on Buying Short Sale Homes Answered

You’ve made it this far, so you’re clearly serious. You see the potential locked inside these complicated deals and you’re ready to tackle the challenges. But let’s be real—you’ve still got questions swirling.

This is where we cut through the noise. Here are the straight, no-nonsense answers to the questions I hear most from investors and homebuyers before they dive into the world of LA short sales.

How Long Does This Really Take?

Patience isn’t just a virtue in this game; it’s a non-negotiable requirement. You can close a standard LA home purchase in a brisk 30-45 days. A short sale, on the other hand, operates on a timeline dictated entirely by the seller’s lender.

Prepare for the long haul. A “quick” short sale might wrap up in 90 days, but it’s far more common for the process to drag on for six months, nine months, or even over a year. The timeline is a messy cocktail of factors: the lender’s internal efficiency (or lack thereof), the complexity of any liens on the property, and how clean your initial offer package was.

The biggest delays often come from something as mundane as an understaffed bank department or lost paperwork. This is why your agent’s role in consistent, relentless follow-up is absolutely critical to keeping your deal from falling into a bureaucratic black hole.

Are Short Sales Always a Better Deal Than Foreclosures?

Not necessarily. They’re two completely different beasts, each with its own unique flavor of risk and reward. Both can offer a path to a discounted property, but the “better deal” depends entirely on your strategy, risk tolerance, and renovation budget.

A short sale property is almost always in better condition. Why? Because the homeowner is usually still living there, acting as a cooperative partner in the sale. They have an incentive to keep the place from completely falling apart.

A foreclosure, on the other hand, is a bank-owned (REO) property that has likely been sitting vacant for months. Vacancy is a property’s worst enemy. It opens the door to neglect, vandalism, and rapid deterioration. The foreclosure process itself can sometimes move faster, but you’re often buying a much bigger project.

- Short Sale: Generally in better shape, but the process is longer and more uncertain.

- Foreclosure: Potentially a steeper discount, but often comes with major repair needs and a more adversarial process (like a public auction).

The better deal is the one that actually lines up with your specific goals.

What Are the Biggest Risks I Should Watch Out For?

When you’re buying short sale homes, the risks are real, but they’re manageable if you know what you’re getting into.

The number one risk is simply timeline uncertainty and deal failure. You could invest months of your time and energy waiting for the lender’s approval, only to have them reject your offer or hit you with a counteroffer that kills the deal’s profitability.

Another huge risk is the property’s condition. Short sales are almost always sold “as-is,” a term that should set off both alarm bells and opportunity bells. The seller is broke; they won’t be making any repairs. If your inspection uncovers a cracked foundation or a fried electrical system, that’s your problem to solve. The lender certainly isn’t chipping in. For anyone navigating their first purchase, a solid first-time house buying checklist can build a foundation of knowledge before you tackle the unique challenges of an “as-is” property.

Finally, watch out for title complications. Multiple liens from second mortgages, unpaid taxes, or contractors can create a tangled web that makes closing the deal incredibly difficult—if not impossible.

Can I Use a Standard FHA or VA Loan for a Short Sale?

Technically, yes, but it’s incredibly challenging and usually a terrible fit. Government-backed loans like FHA and VA come with strict habitability standards, often called Minimum Property Standards. These rules exist to protect borrowers, but they create major hurdles for “as-is” properties.

A short sale with peeling paint, a leaky faucet, or a missing handrail might instantly fail an FHA or VA appraisal. Since neither the seller nor the lender is going to pay for these repairs, your loan gets denied and the deal collapses. It’s just not a good match.

This financing roadblock is exactly why most investors chasing short sales use more flexible funding solutions—the kind designed for properties that need some work.

Investor-Friendly Financing Options:

- Cash: King. It’s the fastest and most certain way to close.

- Hard Money Loans: These lenders focus on the asset’s value, not minor property flaws.

- Conventional Renovation Loans: They build the cost of repairs right into the mortgage, like an FHA 203k loan, but are often more flexible.

Using the right financing is crucial. It’s how you get your deal to the finish line without any last-minute surprises.

The Los Angeles real estate market is tough, but hidden opportunities like short sales offer a path for savvy investors and patient homebuyers to find incredible value. It demands grit, knowledge, and a great team. At ACME Real Estate, we specialize in navigating these complex transactions. If you’re ready to explore what’s possible, let’s connect and make your LA real estate goals a reality. Find out more at https://www.acmexserhant.com.