So, you’re ready to cannonball into the deep end of real estate investing. Awesome. It’s a huge move, and the first question that smacks everyone in the face is always about the money: How do you actually pay for an investment property?

Here’s the deal: forget what you know about getting a mortgage for your own home. When you’re buying an investment, lenders don’t see a hopeful homebuyer; they see a business venture. That means the rules are different, the stakes are higher, and your financial ducks need to be in a perfect, military-grade row.

Let’s cut through the jargon and build a financial roadmap that actually works. This isn’t just theory; it’s your launchpad for building real wealth through property.

Your Starting Point for Investment Property Financing

Before you even think about scrolling through listings, you need to get your financial house in order. Lenders are going to put your finances under a microscope to decide if you’re a safe bet or a risky gamble. Nail these three pillars, and you’re already halfway to the finish line.

The Three Pillars of a Strong Application

Lenders will scrutinize three key areas. Get these right, and you’ll look like the kind of professional investor they’re eager to work with.

- Your Credit Score: For an investment property loan, a good score isn’t just a suggestion—it’s a non-negotiable requirement. Most lenders won’t even talk to you without a score of 680 or higher. Get above 740, and you unlock the VIP room with the best interest rates and terms.

- Debt-to-Income (DTI) Ratio: This number is their peek into your wallet. It shows what percentage of your monthly income is already eaten up by debt payments. For investors, a DTI below 43% is the gold standard. It proves you can handle another mortgage payment without ramen noodles becoming your only food group.

- Cash Reserves: This is a big one. Lenders need to see you have a safety net for their safety net. That means having enough cold, hard cash on hand to cover several months of mortgage payments—principal, interest, taxes, and insurance—for the new property, even if it sits empty for a bit.

Investor Insight: Don’t just aim for the minimum here. Having six to twelve months of cash reserves not only makes you a much more attractive borrower but also gives you a powerful buffer against surprise repairs or a tenant who suddenly ghosts you. It’s your business’s emergency fund. Treat it like one.

Core Financing Options at a Glance

Navigating the world of investment loans can feel like trying to read a map in a foreign language. To simplify things, here’s a quick-and-dirty breakdown of the most common financing methods to help you see where you might fit.

| Financing Method | Best For | Typical Down Payment | Key Challenge |

|---|---|---|---|

| Conventional Loan | Investors with strong credit and financials buying traditional properties (1-4 units). | 20-25% | Stricter qualification requirements than for a primary residence. No cutting corners. |

| FHA Loan (Multi-Unit) | First-time investors willing to live in one of the units (“house hacking”). | 3.5% | You must actually live in one unit, and it only works for properties with 2-4 units. |

| VA Loan (Multi-Unit) | Eligible veterans and service members looking to “house hack” their way to wealth. | 0% | Occupancy rules apply, and it’s an exclusive club for those with VA benefits. |

| Portfolio Loan | Experienced investors with multiple properties or deals that don’t fit the standard box. | Varies (often 25-30%) | Higher interest rates and fees; offered by smaller, more agile lenders. |

| Hard Money Loan | Short-term financing for fix-and-flip projects where speed is the only thing that matters. | 20-30% | Brutally high interest rates and short repayment terms (think 6-24 months). |

This table is just a starting point. Your personal financial situation and investment strategy will ultimately determine the best path forward. Talk to a mortgage broker who specializes in investment properties to explore these options in more detail.

Understanding the Market and the Math

Getting financing isn’t just about qualifying; it’s about making a kick-ass business decision. You need to analyze potential deals like a seasoned pro.

Right now, the U.S. housing market is showing some interesting shifts. According to Zillow data, the inventory of active listings surged by 20.8% year-over-year in April, the largest jump for that month since 2019. This creates pockets of opportunity for savvy investors who are ready to act.

Before you get too far, you have to get comfortable with the numbers. This means understanding Cap Rate in real estate investing and other key metrics that tell you if a deal is actually a deal.

You also need to know exactly what your monthly costs will be. For a complete guide, check out our article on how to calculate mortgage payments. This foundational knowledge is what turns confusion into a confident, actionable plan.

Navigating the Different Types of Investment Loans

When you step into the world of investment financing, you’re leaving the familiar territory of primary home mortgages behind. The loan you get for a rental property isn’t the same as the one for the house you live in—not by a long shot.

Lenders play by a different rulebook when their money is on the line for a business venture, which is exactly what your investment property is. Think of it this way: your primary mortgage is a personal loan for your home. An investment loan is a commercial transaction. This shift in perspective changes everything, from interest rates to down payment requirements.

Let’s break down the specific tools in the investor’s financing toolkit so you know exactly which one to reach for.

The Workhorse: Conventional Investment Loans

For most investors, the conventional loan is the go-to option. It’s the most common type of mortgage for properties with one to four units that you don’t plan on living in yourself. But be prepared for a higher bar to clear.

Lenders view non-owner-occupied properties as a higher risk. If you hit a financial rough patch, you’re far more likely to default on your rental before you stop paying for your own home. To offset this risk, they tighten the screws.

Expect to bring a down payment of at least 20-25% to the table. You’ll also need a solid credit score—often 680 or above—and your interest rate will likely be 0.50% to 1.0% higher than the rates for a primary residence.

Pro Tip: Don’t let the tougher requirements scare you. A conventional loan offers stability with a fixed rate and a standard 30-year term, making it a predictable and powerful tool for building a long-term rental portfolio.

The House Hacking Strategy with Government-Backed Loans

What if you could buy an investment property with a tiny down payment? That’s the magic of “house hacking” using government-backed loans. Honestly, it’s one of the most powerful strategies for new investors looking to get their foot in the door.

The concept is simple: you buy a multi-family property (two to four units), live in one unit, and rent out the others. Because you are an owner-occupant, you can unlock incredible financing terms that are usually reserved for primary homes.

- FHA Loans: Famous for their 3.5% down payment requirement, FHA loans are an absolute game-changer. The rental income from the other units can even help you qualify for the mortgage in the first place.

- VA Loans: For eligible veterans and service members, this is the ultimate hack. VA loans allow you to purchase a multi-family property with 0% down. It’s an unbeatable way to kickstart your real estate journey.

The key catch is the occupancy requirement—you must live in one of the units for a specified period, typically at least one year. But the trade-off is massive leverage and a fast track to becoming a landlord.

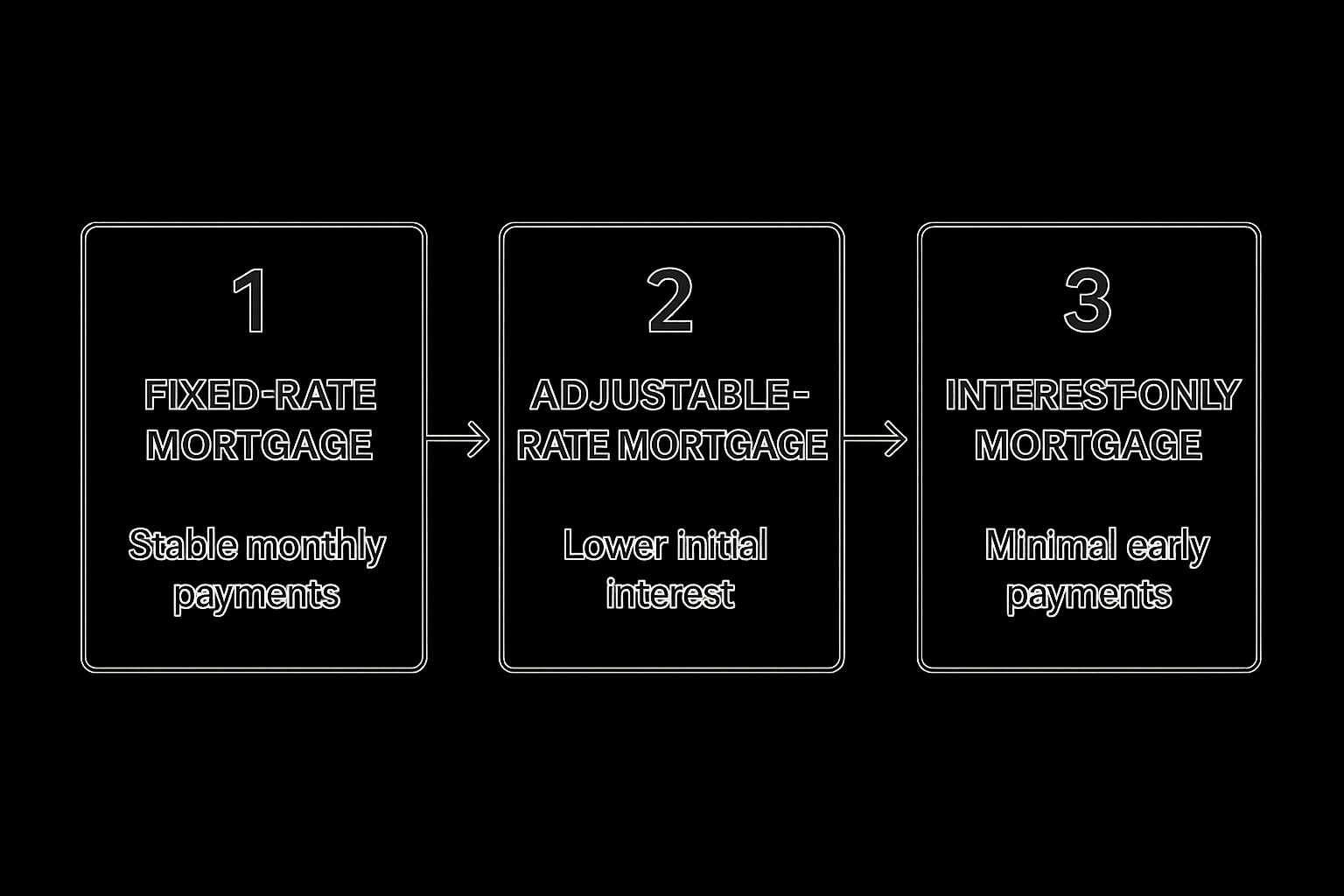

This image breaks down the core structures of mortgage payments, helping you understand how different loan types can impact your cash flow over time. Whether you choose a stable fixed-rate, an initially cheaper adjustable-rate, or an interest-only loan, each has distinct financial implications for your investment strategy.

Comparing Key Investment Loan Features

To help you visualize the trade-offs, this table contrasts the primary features of different investment loan types. Use it to decide which financial product aligns with your investment strategy and timeline.

| Loan Type | Typical Interest Rate | Loan Term | Ideal Investor Profile |

|---|---|---|---|

| Conventional | Prime + 0.5%-1.0% | 15-30 Years | Buy-and-hold investors with solid credit and a significant down payment. |

| FHA (Owner-Occupied) | Varies, Competitive | 30 Years | First-time investors using the “house hacking” strategy with low cash reserves. |

| VA (Owner-Occupied) | Varies, Very Competitive | 30 Years | Eligible veterans and service members looking for a 0% down payment investment. |

| Hard Money | 10%-18% | 6-24 Months | House flippers and investors who need to close a deal extremely quickly. |

| HELOC | Variable, based on Prime | 5-10 Year Draw Period | Existing homeowners leveraging equity for down payments or renovations. |

Choosing the right loan is less about finding the “best” one and more about finding the one that best fits your specific deal and long-term goals.

Advanced Tools for Scaling and Speed

Once you’re ready to scale your portfolio or need to move with lightning speed, traditional loans might not cut it. That’s when you turn to more specialized, flexible financing options designed for seasoned investors and unique situations.

The real estate market is always moving. For the first time in three years, global deal value saw a significant recovery, growing by 11% to reach $707 billion, fueled by strong demand in sectors like multifamily properties. You can explore the full analysis on global private markets from McKinsey. Investors who understand advanced financing are the ones who capitalize on these shifts.

Here are a few tools they use:

- Portfolio Loans: Have multiple properties? Instead of juggling several individual mortgages, a portfolio loan bundles them into one. Lenders who offer these often have more flexible guidelines because they keep the loan “in-house” rather than selling it off.

- Hard Money Loans: When you’re flipping a house and need cash in a week, not a month, a hard money loan is your answer. These are short-term loans from private investors based on the property’s after-repair value (ARV). The trade-off for speed is high interest rates (10-18%) and short terms (6-24 months).

- Home Equity Line of Credit (HELOC): If you have significant equity in your primary residence, a HELOC lets you tap into it. It works like a credit card secured by your home, giving you a revolving line of credit you can use for down payments or renovations. It’s a fantastic way to put an asset you already own to work.

Mastering Down Payments and Lender Requirements

Let’s get one thing straight: financing an investment property is a completely different ballgame. The moment you say “investment,” lenders stop seeing you as a hopeful family looking for a home. You become a business partner.

Suddenly, it’s not just about whether you can afford the mortgage. It’s about whether your deal—and you—are a solid bet. This brings every investor to the same two mountains they have to climb: the huge down payment and the lender’s microscopic inspection of your finances. Forget the 3.5% down FHA loans. For investment properties, you’re playing in a different league, and you need the capital to prove you belong there.

The Down Payment Hurdle: Why 20-25% Is the Magic Number

If you want to finance an investment property, the first number to burn into your brain is 20%. That’s the absolute, rock-bottom minimum down payment most conventional lenders will even look at for an investment loan. In reality, most of them want to see 25%.

Why so steep? It all comes down to risk. Lenders know that if you hit a rough patch financially, the mortgage on your rental property is the first one you’ll probably let slide. A big down payment proves you have serious skin in the game. It makes you a much safer bet.

It also means you can kiss Private Mortgage Insurance (PMI) goodbye. That extra monthly fee tacked onto primary home loans with less than 20% down? Not an option here. Lenders demand that you have significant, immediate equity from day one.

How to Source Your Down Payment (Creatively and Legally)

Staring down a $100,000 down payment for a $400,000 duplex feels like a massive hurdle, I get it. But this is where seasoned investors separate themselves from the rookies. You have to think beyond your checking account.

Here are a few legitimate ways investors build their war chest:

- Tap Your Home Equity: If you already own your home, a Home Equity Line of Credit (HELOC) or a cash-out refinance is one of the most powerful tools for accessing capital. You’re leveraging an existing asset to acquire a new one.

- Bring in a Partner: Don’t have all the cash yourself? Don’t let that stop you. Form a partnership or LLC with someone who does. You can bring the deal-finding hustle and management skills; they bring the capital. Just make sure your operating agreement is rock-solid.

- Use a Self-Directed IRA (SDIRA): For investors with a healthy retirement fund, an SDIRA lets you invest in alternative assets like real estate. The rules are tricky and you’ll need a specialized custodian, but it can be a total game-changer.

- Look for Local Help: This is less common for investors, but some local programs exist. For instance, our guide on down payment assistance programs in California shows what might be available in the Golden State.

Decoding the Lender’s Playbook

Once you’ve got the down payment figured out, you need to brace for underwriting. This is where the lender puts your entire financial life under a microscope. They’re looking for signs of stability and pristine financial health.

Lately, lenders are getting even tougher. MSCI data recently showed a 2% year-over-year dip in global real estate investment volumes. That market caution translates directly to stricter lending criteria. They are not taking chances.

Here’s exactly what they’re zeroing in on:

1. A Higher Bar for Credit Scores

For a primary home, you might squeak by with an average credit score. Not here. For an investment property, lenders want to see a FICO score of 680 at a bare minimum. The best rates and terms? Those are reserved for borrowers with scores north of 740. A high score is non-negotiable proof that you know how to manage debt.

2. Strict Debt-to-Income (DTI) Ratios

Your DTI ratio is simple: it’s your total monthly debt payments divided by your gross monthly income. Lenders use it to see if another mortgage will push you over the edge. Most will draw the line at a 43% DTI, though some might budge for an applicant with a stellar credit score and massive cash reserves.

Investor Takeaway: Here’s a pro tip. Lenders will typically count 75% of the property’s projected rental income toward your qualifying income. They hold back the other 25% to cover vacancies and maintenance. You’ll need a formal rental appraisal from the bank to validate these numbers, but it can make all the difference in getting approved.

3. Cash Reserves: The Ultimate Safety Net

This is the one that trips up most new investors. After you’ve paid the down payment and all closing costs, lenders need to see you have a cash cushion left. This isn’t just a suggestion; it’s a hard requirement.

You’ll need enough liquid cash to cover at least six months of PITI (principal, interest, taxes, and insurance) for the new investment property. This proves you can handle a deadbeat tenant or a broken water heater without defaulting. If you own multiple properties, expect that requirement to climb to 12 months or more.

Walk into a lender’s office with these three areas locked down, and you’ll immediately stand out as a serious investor who understands how the game is played.

How to Find the Right Lender and Secure Your Loan

You’ve sorted out your down payment and your financials are looking sharp. Now for the main event: picking a lender and getting them to say yes.

Resist the urge to just walk into the nearest big bank. Who you borrow from is just as important as how much you borrow. Finding the right lending partner is a make-or-break moment when you’re figuring out how to finance an investment property.

Think of it like building a team for your business. You wouldn’t hire the first person who walked in to manage your property, right? This is a business partnership, and your lender needs to be an expert who lives and breathes investment deals.

The Lender Showdown: Big Banks vs. Local Players

Not all lenders see investment properties the same way. For some, investors are their bread and butter. For others, you’re an annoying distraction from their simple residential mortgage business.

Let’s break down the main players:

- Big National Banks: Sure, you know their names, and their online portals are slick. But they often operate with rigid, one-size-fits-all underwriting rules. If your deal has any nuance, you’re likely to get hit with a soul-crushing “computer says no.”

- Local Credit Unions: These smaller shops are all about relationships. They often keep loans on their own books (called portfolio loans), which gives them the flexibility to look at the whole picture. They know the local market, which is a huge advantage.

- Mortgage Brokers: This is the investor’s secret weapon. A good broker doesn’t work for a single bank—they have a network of dozens of lenders, including niche players who only work with investors. They’re matchmakers who know exactly who will fund your specific type of deal.

Questions to Ask Any Potential Lender

Before you even think about applying, you need to interview your potential lender. Their answers—or how they stumble through them—will tell you everything.

Here’s your interrogation checklist:

- How many investment property loans did you close last year?

- What’s your typical closing timeline for an investor?

- Do you offer portfolio loans, or just conventional stuff?

- Can you use projected rental income to help me qualify? What percentage?

- What are your cash reserve requirements after I close?

A lender who’s in the trenches will fire back sharp, confident answers. If they hesitate or give you vague corporate-speak, walk away. They’re not the one.

Insider Tip: Ask them if they’re familiar with the “Delayed Financing Exception.” It’s a strategy where you buy a place with cash, then immediately do a cash-out refinance to pull your capital back out. If they know what you’re talking about, it’s a huge green flag that they work with serious investors.

Building a Bulletproof Loan Application

Your loan application isn’t just a pile of paperwork; it’s your business plan. You have to present yourself as a competent, professional partner, not just another borrower. A sloppy, half-finished application screams “amateur.”

Your job is to make the underwriter’s job ridiculously easy. Hand them a package so clean and compelling that saying yes is the only logical conclusion.

This means going beyond just tax returns and bank statements. You need to tell a story. Craft a one-page executive summary that lays out the deal: purchase price, estimated rehab costs, and realistic rental income projections backed up with comps from Zillow or Rentometer.

Got landlord experience? Write a short bio highlighting your track record. First-timer? Frame this as your first strategic acquisition in a carefully planned portfolio. This narrative transforms you from a set of numbers into a credible investor.

And if you’re at this stage, it’s the perfect time to get pre-approved. We break down the entire process in our guide on how to get pre-approved for a mortgage.

Finally, never be afraid to negotiate. Once you get a loan estimate from one lender, shop it around. Ask another if they can beat the rate or lower the origination fees. Shaving off even 0.25% on your interest rate can save you tens of thousands over the life of the loan. Locking in the best possible terms is the final, critical step to winning the financing game.

Creative Financing Strategies Beyond the Bank

Sometimes, the perfect deal just doesn’t fit into the neat little box a conventional lender wants to see. When the bank says no, it’s not the end of the road. It’s a sign you need to stop thinking like a borrower and start thinking like a dealmaker.

This is where the real hustle begins. It’s where you unlock opportunities that are completely invisible to investors stuck on the traditional path. Learning how to finance an investment property creatively is a skill that separates the pros from the amateurs.

When the Seller Becomes Your Bank

Imagine negotiating your mortgage terms directly with the person selling you the house. That’s seller financing in a nutshell. In this setup, the property owner acts as the bank, holding the note and collecting your monthly payments.

This strategy is a game-changer when a property has issues that scare off traditional lenders—maybe it needs significant repairs or has an unconventional layout. Sellers who own their property free and clear are often open to this, especially if it means a faster, smoother sale at their asking price.

You get to negotiate everything: the interest rate, the down payment, and the loan term. It requires an ironclad legal agreement drawn up by a real estate attorney to protect everyone, but the flexibility is unmatched.

Tapping into Private Money Lenders

Look around your network. You probably know successful people—doctors, lawyers, business owners—who have capital sitting in low-yield accounts. These individuals are your potential private money lenders. They aren’t banks; they’re investors looking for a better return than the stock market can offer, secured by a tangible asset.

Your job is to pitch them a solid deal. Present the property, the numbers, and a clear plan for how they’ll get their money back, plus a healthy return (typically 8-12% interest).

The Power of the Pitch: When approaching a private lender, don’t just ask for money. Present a professional loan package with comps, a rehab budget, and projected profits. You’re not a borrower asking for a favor; you’re a business partner offering a secure, high-yield investment opportunity.

This method is all about trust and professionalism. Every deal should be documented with a promissory note and a mortgage (or deed of trust), making it a formal, legally binding loan.

The Strength in Numbers: Partnerships and Syndicates

Have your eye on a multi-million dollar apartment complex but only have the capital for a duplex? It’s time to team up. Forming a partnership or a real estate syndicate allows you to pool your money, skills, and resources with other investors to tackle bigger, more profitable deals.

- Partnerships: This could be as simple as you and a friend going in on a property 50/50. One partner might bring the cash for the down payment, while the other brings the expertise to find and manage the property.

- Syndications: This is a more formal structure where a “sponsor” (that could be you) finds a large deal and raises money from a group of passive investors. It’s how investors scale up to commercial properties without needing millions of their own capital.

These alternative methods, along with others like buying real estate in an IRA, definitely require more grit, negotiation, and legal legwork. But they also give you a massive competitive advantage, opening doors to deals that ninety percent of other buyers can’t even touch.

Got a Few More Financing Questions?

You’ve made it through the jungle of loan types, down payments, and lender hoops. But let’s be honest, a few nagging questions are probably still rattling around in your head. That’s not just normal; it’s a sign you’re taking this seriously.

When you’re figuring out how to finance an investment property, the details are everything. I’ve rounded up some of the most common questions I hear from investors, with the straight-up answers you need to get unstuck and move forward.

Can I Really Get an Investment Property Loan with No Money Down?

The short answer is almost always no—at least not in the way most people imagine. A true zero-down loan from a conventional lender for a property you don’t plan to live in is basically a myth. Lenders demand that you have significant skin in the game, which is why that 20-25% down payment is the industry standard.

But that doesn’t mean you’re out of options. You just have to get creative to get a similar result:

- The VA Loan House Hack: This is the closest you’ll get to the real thing. If you’re an eligible veteran, you can buy a multi-family property (2-4 units) with 0% down, live in one unit yourself, and have your tenants pay your mortgage.

- Bring in a “Money Partner”: You find the deal, you manage the property, you do the work. Your partner brings the cash for the full down payment and closing costs. You’re trading sweat equity for their capital.

- Seller Financing: Every once in a while, you’ll find a motivated seller who is willing to act as the bank and finance the entire deal. It’s rare, but when it happens, you can sometimes get in with very little cash upfront.

How Many Investment Property Loans Can I Have at Once?

This is the big question for any investor who wants to scale their portfolio. The answer really depends on who you’re borrowing from.

Fannie Mae, the government-sponsored entity that sets the rules for most conventional loans in the U.S., draws a hard line at 10 financed properties for any single borrower. But here’s the catch they don’t always tell you about: the requirements get brutally strict after your fourth property. For properties five through ten, lenders will demand higher credit scores, lower debt-to-income ratios, and much, much larger cash reserves.

Investor Takeaway: This is where building relationships with smaller banks and portfolio lenders pays off. These lenders often keep their loans “in-house” and don’t have to follow Fannie Mae’s hard 10-property limit. They’ll look at your entire portfolio and your track record as an investor, making them essential partners for anyone serious about growing beyond that ten-loan ceiling.

Does Rental Income Count Toward My Loan Qualification?

Yes, absolutely. In fact, it’s a critical piece of the puzzle that makes scaling possible. But lenders don’t just take your word for what a property will rent for. They have a specific formula to make sure they’re working with a conservative, realistic number.

Here’s how it usually works: A lender will only count 75% of the property’s gross monthly rental income. They automatically write off the other 25% to account for things like vacancies, repairs, and property management fees.

For a new purchase, the lender will order a special appraisal that includes a “Comparable Rent Schedule” to establish the fair market rent for the area. If you already own rental properties, you’ll need to show a history of that income on your tax returns (look for Schedule E) for the lender to count it. It’s a powerful tool that can help you meet those tough DTI requirements and get the green light.

At ACME Real Estate, we believe smart financing is the bedrock of any successful real estate portfolio. Whether you’re buying your first rental or scaling to your tenth, our team has the local know-how and industry connections to guide you through every single step. Ready to turn your investment dreams into reality in Los Angeles? Let’s connect today.