You’ve found the house. Your offer was accepted. It feels like the hard part is over, but before you start picking out paint colors, there’s one last gatekeeper standing between you and the keys: the mortgage underwriter.

This isn’t just a formality. This is the lender’s deep-dive financial background check, a critical moment where they verify every single detail you’ve provided to decide if you’re a good bet for a massive loan. So let’s crack the code on how it all works.

What Is Mortgage Underwriting and Why It Matters

Think of underwriting as the final boss in your home-buying game. A real person—an underwriter—becomes a financial detective, meticulously digging into your credit, your ability to pay, and the value of the house itself. Their goal is brutally simple: protect the lender from risk.

It’s not personal, but it sure feels like it. They’re putting your entire financial story under a microscope to confirm that both you and the house are a sound investment. This is the stage where your homeownership dream gets the final green light—or a red one.

The Underwriter’s Core Playbook

So, how do they make such a huge decision? Underwriters rely on a time-tested framework known as the “Three C’s.” It’s their way of systematically breaking down the risk of lending you hundreds of thousands of dollars.

- Capacity: Can you actually afford this? They’ll scrutinize your income, job stability, and debt-to-income ratio. They need to see that you have enough cash flow to handle the new mortgage payment on top of all your existing bills.

- Credit: What’s your track record with paying people back? Your credit history and score tell the story of how you’ve handled debt in the past. They’re looking for a consistent history of on-time payments and responsible borrowing.

- Collateral: Is the house itself worth what you’re borrowing? The home you’re buying is the collateral for the loan. An independent appraiser has to confirm its market value, ensuring the lender is protected if you default.

The whole process is about connecting the dots. The underwriter is piecing together your financial past (Credit), your present ability to pay (Capacity), and the future value of the asset (Collateral) to make a final call.

To get a clearer picture, here’s a quick breakdown of what each “C” really means for you.

The Three C’s of Underwriting at a Glance

| Pillar | What It Means for You | What an Underwriter Checks |

|---|---|---|

| Capacity | Do you earn enough to comfortably make your payments? | Pay stubs, tax returns, W-2s, employment verification, debt-to-income (DTI) ratio. |

| Credit | Are you reliable when it comes to paying your debts? | Credit score, payment history, bankruptcies, liens, amount of existing debt. |

| Collateral | Is the property a safe investment for the lender? | The property’s official appraisal report, title search, and home inspection results. |

Each piece of this puzzle is critical. A weakness in one area might be offset by strength in another, but all three need to tell a compelling story for your loan to be approved.

How Underwriting Has Changed

While the “Three C’s” are timeless, the how has changed dramatically. What used to be a painfully slow, manual process involving stacks of paper has become incredibly fast.

Today, technology does a lot of the heavy lifting. AI and real-time data analytics now allow lenders to verify information and make decisions in a fraction of the time it once took. To get a sense of just how much things have shifted, you can learn more about the evolution of mortgage underwriting from industry insiders who’ve seen it firsthand.

Decoding Your Financial Profile for Loan Approval

An underwriter’s job is to read your financial story. They aren’t just looking at a pile of numbers; they’re piecing together a narrative to predict how you’ll handle a massive loan. Think of them as a financial detective.

To do this, they zero in on four key chapters of your financial life. The industry calls them the “Four C’s.” Understanding what these mean from an underwriter’s perspective is the key to building an application that doesn’t just get looked at—it gets approved.

Let’s break down exactly what they’re looking for and why it matters so much.

Credit: Your Financial Reputation

Your credit report is your financial reputation on paper. It’s a detailed history of every promise you’ve made to pay someone back and, more importantly, whether you kept it. The underwriter isn’t just glancing at your score; they’re reading the story behind it.

A high score is great, but they’re digging for consistency. A long history of on-time payments for different kinds of credit (like car loans and credit cards) screams reliability. On the other hand, a few recent late payments, accounts in collections, or maxed-out credit cards are massive red flags. It tells them you might be in over your head.

Actionable Insight: Your credit history is more than just a number. It’s the primary evidence an underwriter uses to gauge your reliability. A strong, consistent payment history is your most valuable asset here. Pull your own report before applying to catch and fix any errors.

Capacity: Your Ability to Pay

This is where the rubber meets the road. Capacity is all about whether you can actually handle the proposed mortgage payment on top of everything else you owe. The underwriter has one job here: make sure you won’t be stretched too thin each month.

To figure this out, they calculate your debt-to-income (DTI) ratio. This number compares your total monthly debt payments—including your estimated new mortgage—to your gross monthly income. A low DTI means you have plenty of breathing room. A high DTI signals financial stress.

Lenders generally want to see a DTI ratio below 43%, though some loan programs have different limits. If you want to see where you stand, it’s worth learning how to calculate your debt-to-income ratio and what it means for your approval odds.

Capital: Your Skin in the Game

Capital is the money you’re personally putting on the line. This means your down payment plus any cash you’ll have left over after closing. To an underwriter, this is your “skin in the game.” It’s proof you’re just as invested in this deal as they are.

A bigger down payment accomplishes two critical things:

- It lowers the lender’s risk. The less they have to lend, the smaller their potential loss if you ever default. Simple as that.

- It shows financial discipline. It proves you can save a significant amount of money, which is a powerful indicator of financial responsibility.

Beyond the down payment, underwriters also need to see that you have cash reserves—usually a few months’ worth of mortgage payments sitting in the bank. This is your safety net. It ensures you can still make your payments if you lose your job or face an unexpected emergency.

Collateral: The Property’s Value

Finally, the house itself has to pass inspection. The property you’re buying serves as the collateral for the loan. If you stop making payments, the lender needs to know they can sell the house to get their money back.

This is why a home appraisal is non-negotiable. A licensed appraiser assesses the property to determine its fair market value. The underwriter pores over this report to make sure the loan amount isn’t more than the home is actually worth. They also check for any major health or safety issues that could sink the property’s value.

The house has to be as solid of an investment as you are. Period.

The People Who Decide Your Mortgage’s Fate

Getting a mortgage isn’t a solo mission. It’s more like a team sport, and while you’re the star player, a whole crew of professionals is working behind the scenes to get your loan across the finish line.

Knowing who does what can transform the mortgage underwriting process from a black box of mystery into a collaborative effort. Think of it like a film crew, where each person has a critical role in producing the final blockbuster: your new home. Understanding their jobs helps you ask the right questions and give them what they need, right when they need it.

The Director: Your Loan Officer

Your Loan Officer (LO) is the director of this production. They’re your main point of contact and your guide from the very beginning. The LO’s job is to help you find the right loan, navigate the application, and basically set the strategy for getting your mortgage approved.

A good LO is your advocate, coordinating with the rest of the team to keep your file moving. They anticipate problems before they happen and work with you to solve them long before they ever land on an underwriter’s desk.

The Producer: The Loan Processor

Once your application is in, the Loan Processor steps in. Think of them as the producer—the person who gathers all the pieces needed for the film. They collect, organize, and verify every single document required to build a rock-solid loan file.

This means they’re responsible for:

- Document Collection: Chasing down your pay stubs, bank statements, tax returns, and everything in between.

- File Assembly: Putting it all together into a clean, complete package that tells a clear and convincing financial story.

- Initial Verification: Double-checking details like your employment history and bank balances before the file gets passed up the chain.

The processor’s goal is to give the underwriter everything they need for a smooth review. Your prompt responses to their requests are absolutely essential to keep things on track.

Pro Tip: Your processor is your best friend for a speedy process. When they ask for a document, send it over as quickly and clearly as you can. They want to make your file so perfect that the underwriter has no reason to question it.

The Critic: The Mortgage Underwriter

The Underwriter is the discerning critic who gives the final green light. They are the ultimate decision-maker, hired by the lender to meticulously analyze the risk of lending you money. Using the file the processor built, they do a deep dive into your credit, capacity, and the collateral.

You won’t talk to them directly. Instead, they communicate through your loan officer, often issuing a “conditional approval” with a list of final items needed to close the deal. Their final sign-off is the climax of the entire mortgage process.

The Location Scout: The Appraiser

Finally, the Appraiser is the location scout. They’re an independent, third-party professional brought in to determine the fair market value of the property you want to buy. Their unbiased assessment ensures the collateral—the house itself—is worth the amount you’re borrowing.

The underwriter leans heavily on the appraiser’s report to confirm the property is a sound investment for the lender. The valuation has to support the loan amount for everything to move forward. It’s this whole team, working in concert, that turns your homeownership dream into a reality.

Navigating the Mortgage Underwriting Timeline

Okay, so your loan processor has bundled up your life into a neat little package. Now what? Your file is about to enter underwriting, which for most buyers feels like sending your application into a black hole and just… waiting.

But it’s not a mystery box. It’s actually a straightforward, four-stage journey. Knowing how it works helps you understand the dreaded waiting game and, more importantly, shows you how much power you have to speed things up. Think of it as a relay race—your job is to be ready when the baton comes your way.

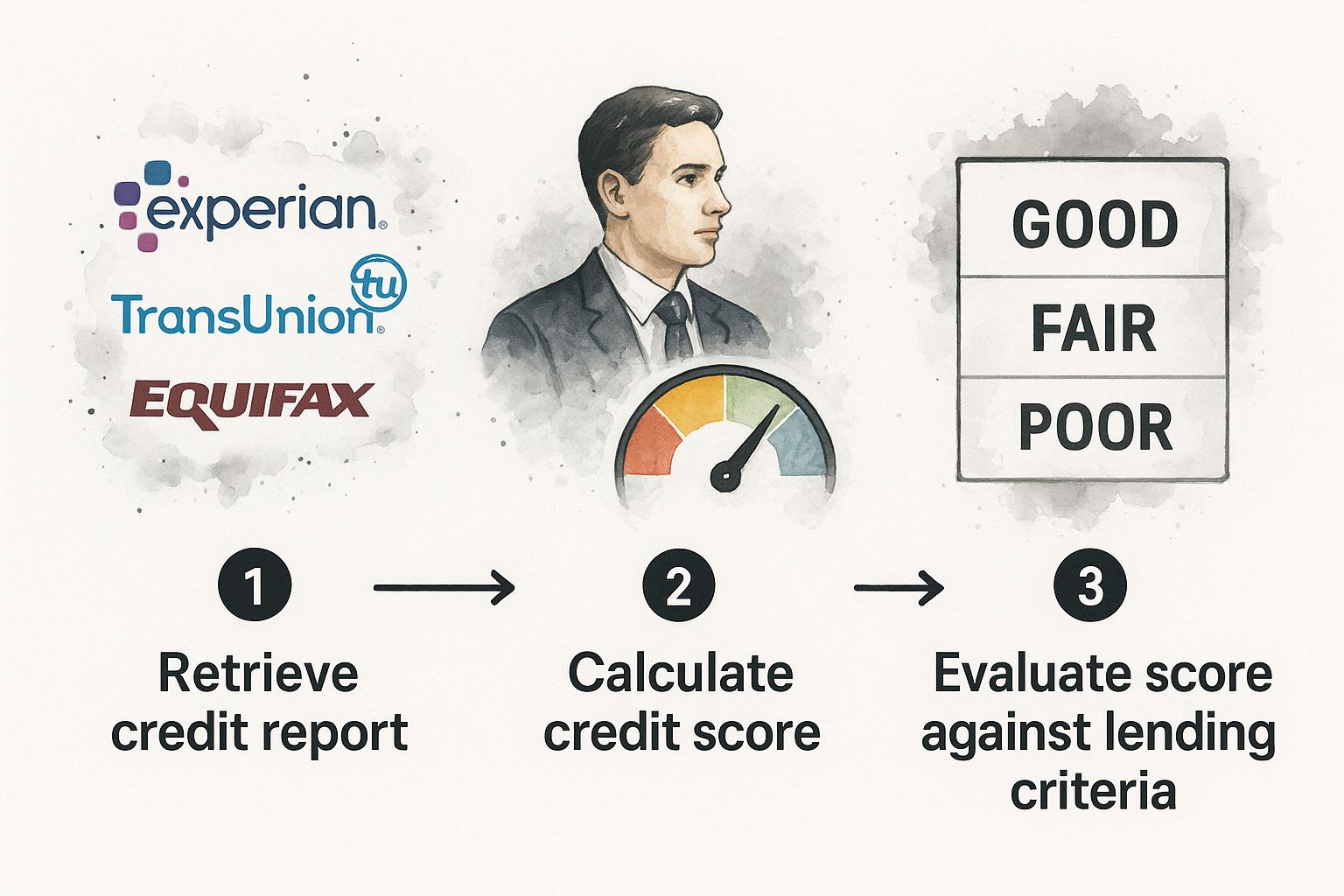

This infographic gives you a quick look at how your credit—one of the first things an underwriter checks—gets sized up at the very beginning of this process.

Essentially, a solid credit profile is the first gate you need to pass through. Get through that, and you’re moving forward with some serious momentum.

Stage 1: The Initial Submission

This is the starting line. Your loan processor has collected all your initial paperwork—pay stubs, bank statements, tax returns—and organized it into a file designed to tell your financial story clearly.

Once they’re confident everything is in order, they officially send it off to the underwriting department. The second your application lands on an underwriter’s desk, the clock officially starts ticking.

Stage 2: The Underwriter’s First Review

An underwriter now opens your file and does their first deep dive. This is where they put your financial life under a microscope, looking at every single detail to assess the lender’s risk. They’ll verify your income, pick apart your credit history, confirm your assets, and go over the property appraisal with a fine-toothed comb.

This review usually takes a few business days. The goal here is to get a “conditional approval.” Getting one is great news. It means the underwriter is on board with approving your loan, as long as you can clear up a few final items, or “conditions.”

A conditional approval isn’t a bad sign; it’s just a to-do list. The underwriter is basically saying, “This looks good, but I need you to clarify these few things before we can sign off.”

Conditions are totally normal. They might ask for your most recent pay stub, a letter explaining that large cash deposit from your aunt, or some context for a recent credit inquiry. This isn’t a red flag—it’s just part of their job to leave no stone unturned.

This level of detail is exactly what keeps the housing market stable. As of early 2025, U.S. banks were servicing roughly 10.9 million residential mortgages, and a staggering 97.6% of them were current and performing. That’s a direct result of solid underwriting.

Stage 3: Clearing Conditions

The ball is now back in your court. Your loan officer will shoot you a list of the conditions from the underwriter. This is where you, your loan officer, and your processor team up to track down and submit whatever they’ve asked for.

Your speed here is everything. The faster you can deliver clear, complete documents, the faster you get to the finish line. Honestly, this is the stage where most delays happen. For more context on where this fits into the grand scheme of things, take a look at our complete home buying process timeline.

Common conditions might include things like:

- An updated bank statement to prove the money for closing is still sitting there.

- A letter of explanation for a gap in your employment history.

- Proof of homeowners insurance for the property you’re buying.

- A final verification of employment, which they do right before closing to make sure you still have your job.

Stage 4: The Final Review and Clear to Close

Once you’ve sent everything back, your file returns to the underwriter for one last look. They’ll go through their checklist, making sure every single condition has been met and every question answered.

If it all checks out, you’ll hear the three most beautiful words in real estate: “Clear to Close” (CTC). It means the underwriter has given the final, official green light. Your loan is fully approved, and the lender is ready to wire the funds. From here, it’s off to the closing department to schedule your signing day and finally get you the keys.

Common Mistakes That Can Derail Your Approval

You’ve navigated the offers, you’ve survived the inspections, and the finish line is finally in sight. But this next stage—underwriting—is where so many buyers accidentally trip themselves up. It’s the home stretch, and the best advice anyone can give is to put a giant “do not disturb” sign on your entire financial life.

Any sudden moves can send an underwriter into a panic and put your approval in jeopardy. It’s not about being perfect. It’s about being predictable. Underwriters hate surprises, so here’s how to avoid the self-inflicted wounds that can kill your loan at the eleventh hour.

The New Debt Nightmare

This is the big one. We see it happen all the time. You’re pre-approved for the house, so you figure, “What’s the harm in financing a new car or some furniture for the living room?” Wrong. It’s a massive deal.

Taking on new debt of any kind—a car loan, a personal loan, even just running up a credit card for new appliances—completely changes your financial snapshot. It immediately jacks up your debt-to-income (DTI) ratio, which is the single most important number the underwriter used to approve you in the first place.

That new monthly payment could be the one thing that pushes your DTI over the lender’s limit, turning a slam-dunk approval into a soul-crushing denial. The rule is brutally simple: from the moment you apply to the moment you close, do not open any new lines of credit. The new sectional can wait. We promise.

The Job Hop Conundrum

Thinking of switching jobs for a better title or a bigger paycheck? While that’s normally a fantastic career move, doing it in the middle of underwriting is like trying to change horses while crossing a river. Underwriters are obsessed with stability, and your employment history is their proof that you have it.

Changing jobs, especially if you’re moving from a salaried W-2 position to a commission-based or self-employed role, creates a colossal documentation headache. The underwriter has to start from square one, re-verifying everything. If your new income structure looks even slightly less predictable, it could torpedo the entire loan.

The Golden Rule: If you absolutely must change jobs, call your loan officer before you even think about giving notice. They can walk you through how to manage the transition without blowing up your mortgage approval.

The Mystery Money Problem

Nothing sends an underwriter into a tailspin faster than seeing a large, undocumented cash deposit pop up in your bank account. It raises immediate red flags about where that money came from. Is it an undisclosed loan from your uncle? Is it cash you’ve been stashing under the mattress?

Every single dollar you use for your down payment and closing costs has to be sourced and seasoned. That’s industry speak for the lender needing to see a clear paper trail of where it came from and proof that it has been in your account for a while (usually at least 60 days).

If a family member helps you out, it needs to be properly documented with a gift letter that explicitly states the money is a gift, not a loan you have to repay. Shuffling big piles of cash around without documentation is one of the fastest ways to get your file kicked to the bottom of the pile—or denied altogether.

The lending world is always in flux. After a historic boom in mortgage originations that topped $4 trillion in 2021 thanks to rock-bottom rates, the market has tightened its belt. Rising interest rates have forced lenders to be far more strict, making financial consistency more critical than ever. You can dig into recent market trends by checking out Ginnie Mae’s global market analysis.

By sidestepping these common mistakes, you’re handing the underwriter a clean, consistent, and predictable file. You’re making their job easy, and that’s the real secret to a smooth and successful closing.

How to Prepare Your Application Like a Pro

The secret to a smooth underwriting experience isn’t luck. It’s preparation.

Think of it this way: you’re giving the underwriter a neatly organized puzzle that’s already been solved. Your goal is to make their job so easy that saying “yes” is the only logical next step.

When you get your financial house in order before your file ever lands on their desk, you sidestep the stressful, last-minute scrambles that kill deals. This approach shows you’re a serious, organized borrower—exactly the kind of client lenders want.

Assemble Your Financial Toolkit

First things first, gather your documents. Don’t wait for your loan officer to send a frantic email asking for paperwork you haven’t seen in years. Having everything ready to go shows you mean business and keeps the process moving.

Here’s a basic pre-submission checklist:

- Proof of Income: Typically, this means your last two years of W-2s and tax returns, plus your most recent 30 days of pay stubs.

- Bank Statements: Have at least two months of statements for all your accounts—checking, savings, investment—ready to go. Be prepared to explain any large or unusual deposits.

- Identification: A clear copy of your driver’s license and Social Security card is standard.

Getting this stuff together is a huge first step. If your income is complex (self-employed, rental properties), it’s worth understanding the crucial role accountants play in business financing and loan applications to ensure everything is accurate and complete.

The Power of Proactive Explanations

Underwriters are trained to spot inconsistencies. Instead of waiting for them to question a blemish on your record, get ahead of it with a Letter of Explanation (LOE). This is just a simple, straightforward letter that provides context for anything that might look odd.

Did you have a late credit card payment two years ago? Write a brief LOE explaining what happened and how you’ve since maintained a perfect record. Is there a random, large deposit from a relative? Attach a gift letter.

Actionable Insight: Transparency is your best friend. A well-written Letter of Explanation turns a potential red flag into a non-issue by answering the underwriter’s questions before they even have to ask them.

This strategy frames you as a responsible and honest applicant, building trust from the start. It shows you’ve reviewed your own file and are prepared to address any potential concerns.

This level of readiness is the same mindset you need before the house hunt even begins. For a deeper dive into that initial phase, our guide on how to get pre-approved for a mortgage is a great resource.

By presenting a clean, organized, and transparent file, you’re not just submitting an application; you’re making a powerful case for your approval. You’re setting yourself up as the ideal loan candidate who is ready to close.

Answering Your Toughest Underwriting Questions

Even when you understand the basics, the underwriting process can feel like a total black box. You hand over your entire financial life in a stack of PDFs, send it into the ether, and then… you wait. It’s nerve-wracking. Let’s pull back the curtain and tackle the questions that really keep people up at night.

How Long Does This Actually Take?

This is the big one, isn’t it? There’s no magic number, but most of the time, you’re looking at a few days to a couple of weeks. The real timeline comes down to two things: how complicated your finances are and how fast you get back to them.

If you’ve got a straightforward W-2 job and a clean file, you might fly through in 48-72 hours. But if you’re self-employed with multiple businesses, it’s going to take longer. The underwriter has to connect every dot. The one thing you can control is your response time. Every day you delay sending a document is another day added to the clock.

What Does “Conditional Approval” Really Mean?

Getting a conditional approval is a huge win. Seriously, pop a bottle of something. It means the underwriter has gone through your file and has basically said, “Yes, we want to give you this loan, but first you need to do these last few things.” It’s not a maybe; it’s a to-do list.

Think of it this way: The underwriter is saying, “Everything looks solid, but I just need your latest bank statement and proof you’ve set up homeowner’s insurance.” Once you check off those last items, you get the final “clear to close.”

Seriously, Why Do They Need So Much Paperwork?

We get it. It feels like they’re asking for your third-grade report card. But every single document request has a reason behind it. Underwriters have a legal and professional duty to build a completely bulletproof case for your loan.

Underwriters are basically financial detectives. They aren’t trying to make your life harder; they’re meticulously proving to the lender—and to federal regulators—that you’re a responsible borrower who can handle this mortgage. They have to leave no stone unturned.

What Happens If My Loan Gets Denied?

Getting a denial is a gut punch, but it’s not always the final word. The very first thing you need to do is ask your loan officer for the exact reason. Lenders are required by law to tell you why.

More often than not, a denial is based on something fixable. Maybe your debt-to-income ratio was just a little too high, or a weird error popped up on your credit report. Once you know what the problem is, you can build a game plan. You can fix the issue, strengthen your application, and try again when you’re in a better position. It’s a setback, not a dead end.

Navigating the complexities of the Los Angeles real estate market requires a guide who knows every neighborhood and every step of the process. ACME Real Estate is here to be your expert partner from your first house tour to the final closing day. Visit us at https://www.acmexserhant.com to start your journey.