Let’s cut through the jargon. Fair market value (FMV) isn’t some number pulled out of thin air or what a seller wishes they could get. It’s the price a home would realistically sell for on the open market.

It’s that sweet spot where a buyer who’s done their homework and a seller who’s ready but not desperate shake hands. Think of it as the market’s natural equilibrium—the real-deal price for a property under normal conditions.

Decoding Fair Market Value for Your Home

Ever tried to figure out what a vintage muscle car is really worth? It’s not just the owner’s asking price, and it’s definitely not the lowball offer from someone hoping for a steal. The car’s true value is found when an enthusiast who knows its history, condition, and rarity meets a seller who is willing to part with it for the right price.

That’s exactly how fair market value works in real estate. It’s not a static price tag but a living, breathing consensus. This number is the foundation for almost every major financial decision you’ll make as a homeowner.

Why FMV Is the Core of Real Estate

Getting a grip on fair market value is non-negotiable because it touches every part of your financial life.

- Property Taxes: Your city or county government uses a form of FMV (often called an “assessed value”) to figure out how much you owe in property taxes each year.

- Homeowners Insurance: Insurers need to know your home’s FMV to make sure you’re covered for the right amount if disaster strikes.

- Getting a Mortgage: Lenders won’t just take your word for it. They require an appraisal—a professional’s formal opinion of the FMV—to decide how much money they’re willing to lend you.

At its core, Fair Market Value is a hypothetical handshake. It’s the price that gets hammered out under ideal conditions, where everyone is informed, nobody is under duress, and the deal makes sense for both sides.

This isn’t some niche real estate term; it’s a globally recognized concept that underpins multi-trillion-dollar markets, from homes to corporate assets. Industry standards define it as the price an asset would fetch when both buyer and seller are acting rationally and without compulsion. If you want to see how this plays out in the business world, you can learn more about Fair Market Value principles.

This shared understanding creates a transparent and predictable marketplace, turning what could be a chaotic negotiation into a transaction grounded in reality.

Before we dive deeper, let’s break down the key ingredients of FMV into a simple summary.

Fair Market Value Core Principles at a Glance

This table boils down the essential concepts that define a true fair market value transaction.

| Principle | What It Really Means |

|---|---|

| Voluntary Parties | No one is being forced to buy or sell. The seller isn’t facing foreclosure, and the buyer isn’t in a “must-buy-today” panic. |

| Informed Decision | Both the buyer and seller have reasonable knowledge of the property’s condition, the local market, and recent comparable sales. |

| Open Market | The property has been available to the public for a reasonable amount of time, giving potential buyers a fair shot at it. |

| Arm’s Length | The buyer and seller are independent parties. A sale between family members at a discount doesn’t count as FMV. |

| No Undue Pressure | Neither side has a gun to their head. There are no external pressures forcing a quick or disadvantageous deal. |

Think of these principles as the rules of the game. When all these conditions are met, the resulting sale price is the closest you can get to a property’s true fair market value.

The Three Main Methods for Calculating FMV

So how do appraisers and agents actually land on that magic number? It’s not about gut feelings or throwing a dart at a board. Pinpointing what a property is truly worth involves a mix of art and science, grounded in three battle-tested valuation methods. Getting a handle on these approaches helps you see a property through the eyes of an expert.

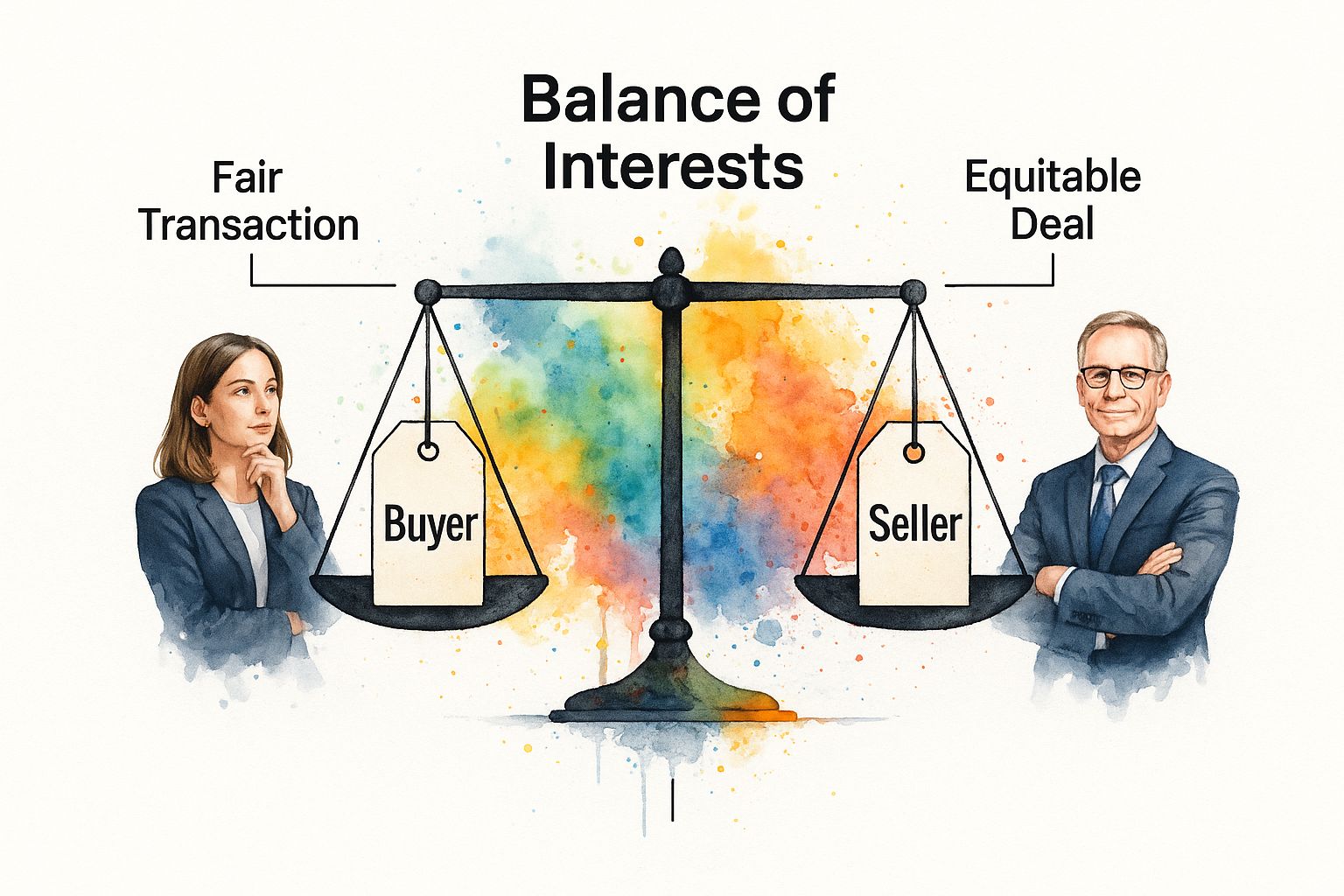

This image really nails the core concept: fair market value is that perfect balance point between what a willing buyer will pay and what a willing seller will accept.

It’s not one side winning. It’s a point of mutual, informed agreement where a deal can actually happen in a competitive market.

The Market Approach (Or Sales Comparison)

This is the bread and butter for residential real estate, and it’s exactly what it sounds like. You’re simply comparing the property in question to similar homes that have recently sold in the same area. We call these the “comps.”

Think of it this way: if three nearly identical houses on your block all sold for around $800,000 in the last few months, your home’s value is almost certainly in that same ballpark. Of course, an appraiser will then make adjustments for key differences:

- Upgrades: Did your neighbor spring for a brand-new kitchen while yours is straight out of the 90s?

- Condition: Is one home in pristine, move-in shape while another clearly needs a new roof?

- Size: They’ll also adjust the value up or down for differences in square footage and lot size.

This method gives you a powerful, real-world snapshot of what buyers are actually willing to pay right now. To see how this plays out in the real world, check out our guide on how to determine home value for a much deeper dive.

The Cost Approach

But what happens if the property is totally unique—like a one-of-a-kind custom build with no good comps, or a brand-new building? That’s where the Cost Approach comes in. This method calculates value by asking a simple question: “What would it cost to build this exact same property from scratch today?”

The formula is pretty straightforward:

- First, you estimate the cost of the land.

- Next, you calculate the cost to construct the building at today’s prices.

- Finally, you subtract depreciation for any wear and tear or outdated features.

The Cost Approach basically sets an upper limit on value. A buyer is never going to pay more for an existing property than it would cost them to just build a brand-new equivalent next door.

You’ll see this method used all the time for new construction, public buildings like schools, or properties with such unique features that finding good comps is next to impossible.

The Income Approach

The first two methods work great for the home you live in, but what about a duplex, an apartment building, or a commercial property? For investment properties, the Income Approach is king. This method values a property based on one thing: how much money it can generate.

It looks at hard numbers like rental income, vacancy rates, and operating expenses to determine the property’s net operating income (NOI). Investors use that NOI figure to decide what the property is worth to them as a cash-flowing asset. The higher the potential income, the higher the fair market value. Simple as that.

How Market Factors Impact Your Property Value

A property’s fair market value is anything but static. Think of it as a living number, one that breathes with the rhythm of the market. While the size and condition of a house are obvious value drivers, the real story is often told by powerful forces outside your four walls. These are the factors you can’t control but absolutely need to understand. They can secretly boost or quietly sabotage a home’s worth.

Imagine two nearly identical homes in the same city but different neighborhoods. One might see its value climb steadily while the other stagnates. Why? It’s all about the invisible influencers—the local and economic currents swirling around the property.

These external forces are the secret ingredients that determine whether a property’s value sizzles or fizzles over time.

The Hyper-Local Influencers

That old saying “location, location, location” is more than a cliché; it’s the fundamental truth of real estate. The amenities and infrastructure in a community play a huge role in shaping desirability, which directly fuels what a home is worth.

Consider these game-changers:

- Community Amenities: Proximity to well-kept parks, walking trails, libraries, and community centers adds a layer of appeal that buyers are absolutely willing to pay for.

- Infrastructure Projects: News of a new light-rail station or highway expansion can send property values soaring as an area becomes more accessible and convenient.

- School District Ratings: For many families, this is a top consideration. Homes in sought-after public school districts often command a premium.

- Zoning Changes: These local laws dictate what can be built where. A change allowing more shops nearby could increase walkability and value, or it could create unwanted noise and traffic that hurts it. It’s a double-edged sword.

Economic and Market-Wide Forces

Now, let’s zoom out. Broader economic trends create the waves that lift or lower all boats in the market. These are the big-picture factors that set the stage for every single transaction.

Take mortgage interest rates, for example. They have a direct and immediate impact on what a buyer can afford. When rates are low, buyers have more purchasing power, which tends to push prices up. When rates climb, that power shrinks, often cooling down the market and dragging values with it.

The overall health of the real estate market—whether it’s a seller’s, balanced, or buyer’s market—dictates the entire negotiation landscape. This dynamic shapes everything from listing strategies to the final sale price.

The desirability of a location is paramount, and its growth potential is a key piece of the puzzle. If you’re looking at a specific high-growth area, getting an in-depth homebuilder’s perspective on market conditions in Cape Coral can show you how the pros analyze these factors on the ground.

Understanding these dynamics is critical, especially when you find yourself in a situation with more listings than interested buyers. You can learn more about navigating this exact scenario in our guide on what is a buyer’s market.

Key Factors That Push FMV Up or Down

To make it simple, we’ve broken down the key influencers that can either work for you or against you when it comes to your home’s value. Think of these as the tailwinds and headwinds of the real estate market.

| Value-Boosting Factors | Value-Reducing Factors |

|---|---|

| Strong local job market | High unemployment or major company layoffs |

| Low mortgage interest rates | Rising mortgage interest rates |

| Proximity to highly-rated schools | Poorly performing school districts |

| New infrastructure (transit, highways) | Lack of public transportation or congested roads |

| Walkable to shops, restaurants, and parks | High crime rates or visible neglect in the neighborhood |

| Positive zoning changes (e.g., new community center) | Negative zoning changes (e.g., industrial plant nearby) |

| High demand with low housing inventory (Seller’s Market) | Oversupply of homes for sale (Buyer’s Market) |

Seeing these factors laid out side-by-side makes it clear how a property’s value is a delicate balance. A great house in a neighborhood with failing schools and rising crime will struggle, while a modest home in a booming, amenity-rich area can see its value skyrocket.

FMV Compared to Assessed and Appraised Value

In the real estate world, you’ll hear the word “value” thrown around constantly, but not all values are created equal. It’s a common mistake to think “Fair Market Value,” “Assessed Value,” and “Appraised Value” are just different names for the same thing. They’re not—and confusing them can be a costly error.

Think of them as different tools for entirely different jobs. Each one spits out a number, but the purpose behind that number changes everything.

Assessed Value: The Tax Man’s Number

That property tax bill you get in the mail every year? The number it’s based on is the assessed value. This figure exists for one reason and one reason only: for your local municipality to calculate how much you owe in property taxes.

You’ll almost always find that the assessed value is lower than a home’s actual fair market value. Why? Tax assessors often use a percentage of the market value and might only reassess properties every few years. It’s a fiscal tool, not a reflection of what your home could sell for on the open market today.

Appraised Value: A Professional Opinion for a Specific Goal

An appraised value is a licensed professional’s formal, data-backed opinion of what a property is worth. This isn’t just a casual estimate; it’s a detailed report created for a specific client and purpose—most often, for a lender to approve a mortgage.

When you’re buying a home, the bank needs to make sure the property is actually worth what you’ve agreed to pay for it. The appraiser’s number protects the bank’s investment. This valuation is also what makes or breaks an appraisal contingency, a critical safety net for buyers.

While an appraiser’s goal is to nail down the Fair Market Value, their valuation is a snapshot in time created for one client: the lender. In a fast-moving market, this can sometimes lead to a disconnect between the appraised value and the agreed-upon sale price.

This disconnect is what’s known as an “appraisal gap.” To get a better handle on this, you’ll want to read up on what to expect as appraisal gaps grow. It will prepare you for situations where the appraisal comes in lower than what you offered.

Putting Your Knowledge of FMV into Action

Understanding fair market value is way more than just a real estate trivia point. It’s a financial superpower that shows up during some of the biggest moments in your life. When you have a solid grasp of what your property is worth on the open market, you can make smarter decisions, save a ton of money, and manage your assets with real confidence.

Think of FMV as a key that unlocks multiple doors. It’s the number that lets you challenge your tax bill or tap into your home’s equity. Knowing it empowers you to act, not just react to what others tell you your property is worth.

FMV in Everyday Financial Planning

Let’s step away from the classic home sale scenario for a minute and look at where else FMV pops up. These situations show why knowing your property’s value is non-negotiable for smart financial management.

- Property Tax Assessments: Your local government uses its own version of FMV (the “assessed value”) to figure out your property tax bill. If you think their number is way off compared to what similar homes are selling for, you can appeal it. A successful appeal could lower your tax bill and save you thousands over time.

- Home Equity Lines of Credit (HELOCs): Applying for a HELOC? The first thing the lender does is determine your home’s FMV to decide how much they’re willing to lend you. A higher, well-supported FMV can give you access to a much larger line of credit for renovations, investments, or whatever else you have planned.

Securing Your Assets and Legacy

The importance of FMV goes way beyond day-to-day finances. It’s a critical piece of the puzzle for long-term planning, like protecting your family’s future.

A property’s Fair Market Value is a foundational data point for everything from insurance coverage to estate settlement. Getting it wrong can have significant, long-lasting financial consequences.

Take estate planning, for instance. An accurate FMV is required to value a deceased person’s assets for tax purposes and ensure everything is divided fairly among the heirs. This isn’t a new concept, either. The legal definition of Fair Market Value was actually formalized by the IRS to create consistency in tax and estate law. You can explore how FMV is officially defined to see how deep the history goes.

It’s just as crucial for homeowners insurance. Your coverage needs to match the FMV of your home’s structure, not just what you paid for it. If your valuation is too low, you could find yourself massively underinsured and facing huge out-of-pocket costs after a fire or natural disaster.

And in a divorce settlement, FMV is the basis for dividing marital assets, including the family home. An unbiased, accurate valuation is the only way to guarantee a fair separation of property. In every one of these cases, knowing your FMV isn’t just helpful—it’s absolutely essential.

A Few More Questions About Fair Market Value

We’ve unpacked a lot, but let’s be honest—the real estate world can still feel like trying to nail jello to a wall sometimes. It’s completely normal to have a few questions rattling around.

So, let’s cut through the noise and tackle the most common ones. Think of this as your final, rapid-fire round to make sure you’re ready for whatever comes next.

Is Fair Market Value the Same as the Listing Price?

Not even close. This is a big one, so listen up. A listing price is the seller’s opening move, their strategic first offer. It’s a number cooked up with their agent, influenced by how fast they need to sell, and, frankly, sometimes a healthy dose of wishful thinking.

Fair market value, on the other hand, is what the market will actually bear, based on cold, hard data. The listing price is the invitation to the dance; the final sale price is usually what lands much closer to FMV. Sure, in a crazy seller’s market, a bidding war can push the price over FMV, but the opposite is just as true when things cool down.

How Often Does a Home’s Fair Market Value Change?

All the time. Constantly. FMV isn’t some fixed number you look up once and tattoo on your arm. It’s alive, shifting day by day with the pulse of the market.

It’s tied to a whole slew of factors that are always in motion:

- Mortgage Rate Swings: A tiny bump or dip in interest rates changes what buyers can afford, which directly impacts what they’re willing to pay.

- Local Inventory: A sudden flood of new listings can cool things off, while a drought of homes for sale can send prices soaring.

- Economic Vibes: The bigger picture matters. Job growth, consumer confidence—it all trickles down to the housing market.

- The Seasons: Most markets have a rhythm. The spring frenzy is a totally different beast from the winter slowdown.

This is exactly why a comp from six months ago might as well be from another decade. Your home’s value is always evolving right along with the world outside your door.

Can I Figure Out My Home’s FMV Myself?

You can absolutely get in the ballpark, and you should. Playing around with online valuation tools and digging into recent sales in your neighborhood is a smart first step. It gives you a feel for the landscape.

A good real estate agent can dial it in further with a Comparative Market Analysis (CMA). That’s a much more detailed, street-level report that’s an incredible tool for getting a real sense of the market.

But here’s the bottom line: for anything official—getting a mortgage, settling an estate, fighting your property taxes—you need a formal appraisal. A licensed appraiser gives an unbiased, legally sound opinion of value that banks and government bodies actually trust.

Does Emotional Attachment Influence Fair Market Value?

This is where things get tricky, but the straight answer is no. All those decades of happy memories a seller has in their home? That can definitely inflate their asking price. But those feelings are worth exactly $0 when it comes to the actual fair market value.

FMV is a creature of data—it’s what a logical, informed buyer is willing to pay. Now, can a buyer fall head-over-heels for a place and pay a premium because it just feels right? Of course. But that overpayment doesn’t magically increase the property’s underlying FMV. It just means that one specific buyer was motivated by something more powerful than the numbers.

Trying to make sense of fair market value is a lot easier when you have an expert in your corner. Whether you’re buying, selling, or just trying to get a handle on your property’s potential, ACME Real Estate brings the data-driven insights and street-level knowledge you need. Let us help you turn your real estate goals into a reality. Explore your options with us today.