To figure out a property’s rental yield, you divide the annual rent you collect by what you paid for the place, then multiply that by 100. Boom. That’s your gross rental yield—a quick and dirty snapshot of an investment’s income potential before expenses crash the party. Getting a handle on this number is the first real step from just owning property to thinking like a strategic investor.

Why Rental Yield Is a Metric You Can’t Ignore

Think of rental yield as your investment’s pulse. It’s a single percentage that tells you exactly how hard your money is working for you. In a world of slick property listings and emotional buys, this number cuts right through the noise to show you the raw earning power of an asset. Without it, you’re flying blind, trying to compare a downtown condo to a suburban duplex without any real, objective yardstick. It’s the difference between guessing and knowing.

Making Smarter Decisions with Cold, Hard Data

Once you know how to calculate rental yield, you can finally see the difference between a property that just looks good online and one that will actually put cash in your pocket month after month. It’s a universal tool that lets you analyze any deal, anywhere, using the same clear standard. And you don’t need a PhD in finance to use it.

This metric is non-negotiable for a few key reasons:

- Objective Comparisons: It levels the playing field, letting you weigh multiple properties against each other, regardless of price point or location.

- Performance Tracking: It’s a pure measure of efficiency, showing you the return you’re getting from rent alone.

- Goal Setting: It helps you define what a “good” investment looks like for you and filter out the deals that don’t match your strategy.

Rental yield is the financial heartbeat of your portfolio. A strong yield points to healthy cash flow. A lower yield might mean the property’s value is more about future appreciation than immediate income. It’s all part of the story.

While rental yield zeroes in on income, it works hand-in-hand with other critical numbers. For another angle on a property’s performance, you should check out our guide on how to calculate cap rate. Understanding both gives you a much fuller, more accurate picture of an asset’s financial health.

At the end of the day, rental yield isn’t just a number. It’s a tool for building a stronger, more profitable real estate portfolio built on logic, not luck.

Gross Rental Yield: Your First Gut Check

When you’re sifting through what feels like hundreds of property listings, you need a fast way to weed out the duds. That’s where the gross rental yield calculation comes in. Think of it as your back-of-the-napkin formula for a quick gut check. It gives you an instant read on a property’s income potential compared to its price, long before you start digging into the nitty-gritty expenses.

The beauty is in its simplicity. It only cares about two things: how much it costs and how much it brings in.

Running The Numbers On Gross Yield

To find the gross rental yield, you just take the total annual rent and divide it by what you paid for the property. Multiply that number by 100, and you’ve got your percentage.

Formula: (Annual Rental Income ÷ Property Purchase Price) x 100 = Gross Rental Yield

Let’s put this into a real-world scenario. Say you’re eyeing a condo with a $400,000 price tag. After checking out comparable rentals in the area, you’re confident you can lease it for $2,500 a month.

- First, get the annual income: $2,500/month x 12 months = $30,000

- Then, do the math: ($30,000 ÷ $400,000) x 100 = 7.5%

Just like that, you know the gross rental yield is 7.5%. This single number lets you quickly compare this condo to another one on the market, giving you a true apples-to-apples baseline to work from.

Keep in mind, this is a high-level view. Gross yield intentionally ignores all the other costs—taxes, insurance, maintenance, you name it. We’ll get into those later to figure out your actual profit.

Still, this quick calculation is invaluable for that first pass. In the United States, the average rental yield can fluctuate, but it’s recently been in the range of 8.1%, a number influenced by a housing shortage that’s pushing rental demand through the roof. You can discover more insights about U.S. rental market dynamics on AmericaMortgages.com. Knowing this context helps you see if that 7.5% is even in the right ballpark for the current market.

Mastering this first step lets you confidently filter out the weak contenders before you waste any time on a deeper financial dive.

Finding Your True Profit with Net Rental Yield

While gross yield gives you a quick snapshot, it’s the net rental yield that tells the real story. This is the number professional investors live by because it reveals your true profit after all the bills are paid. It moves beyond simple math and forces you to account for every single operating expense that nibbles away at your revenue.

Ignoring these costs is a classic rookie mistake. I’ve seen two properties with identical gross yields produce wildly different net returns once the realities of ownership kick in. This is where the pros separate themselves.

Peeling Back the Layers to Find Your Net Yield

To calculate net rental yield, you subtract all your annual operating expenses from your annual rent. Then, you divide that net income figure by the property’s purchase price. This gives you a much more realistic picture of your investment’s actual performance.

This is where meticulous record-keeping becomes your superpower. You have to track every dollar going out the door.

- Property Taxes: A non-negotiable and often significant expense.

- Homeowners Insurance: Essential protection that absolutely impacts your bottom line.

- Routine Maintenance and Repairs: From leaky faucets to lawn care, these costs always add up. Don’t underestimate them.

- Vacancy Reserves: Smart investors set aside funds (usually 5-10% of gross rent) for those inevitable months the property sits empty.

- Management Fees: If you hire a property manager, this is a major operational cost. The property management cost per month is a perfect example of an expense that gets missed in a simple gross calculation.

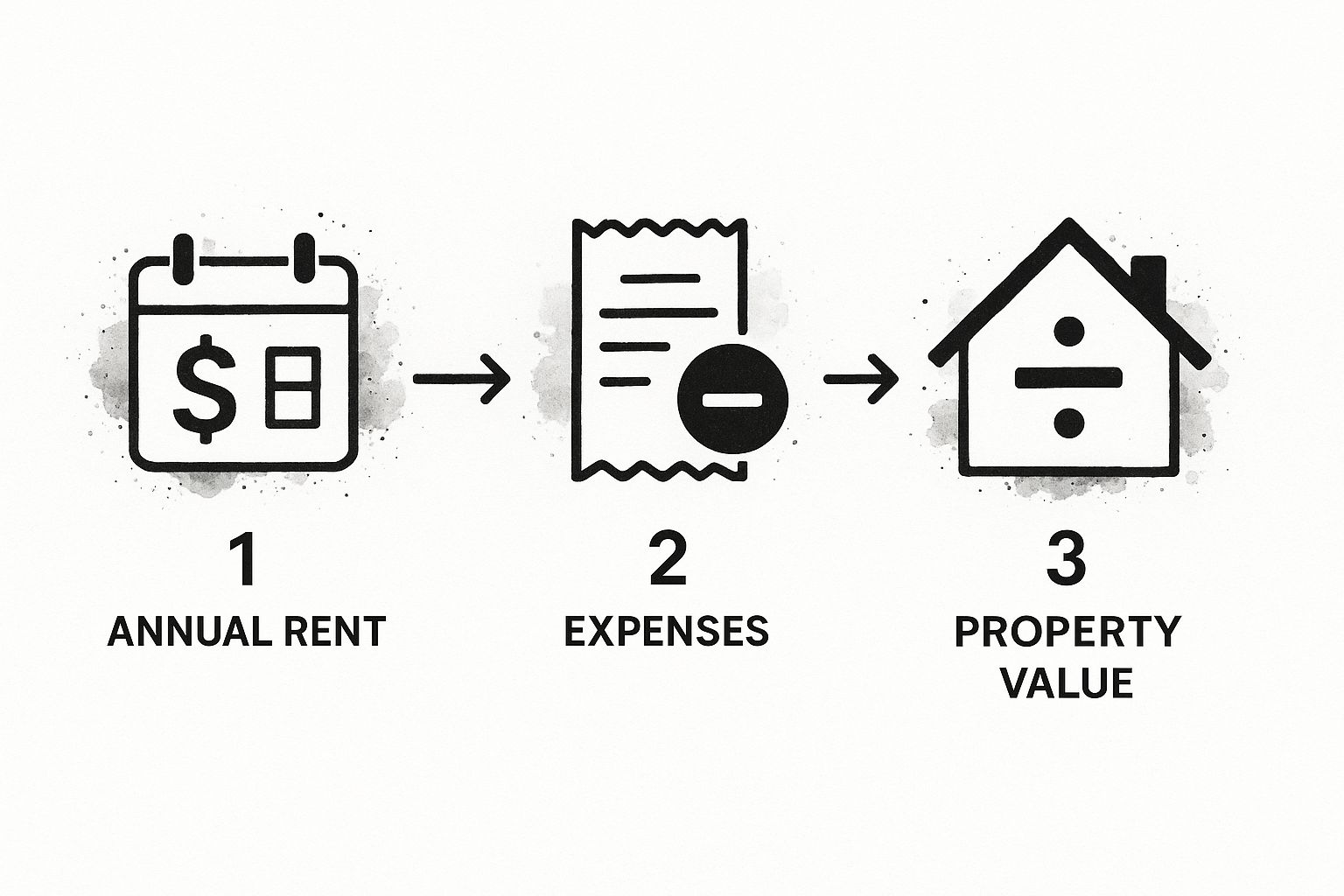

This visual breaks down the simple flow of the net rental yield calculation.

The process is pretty straightforward: annual rent comes in, expenses go out, and what’s left is measured against what you paid for the property.

Net Yield in Action: A Tale of Two Condos

Let’s go back to our $400,000 condo that brings in $30,000 a year in rent. Imagine we have two of them. Both have a 7.5% gross yield on paper, but their net yields tell completely different stories.

Condo A (Newer Build)

- Annual Rent: $30,000

- Annual Expenses (taxes, insurance, low HOA): $6,000

- Net Income: $30,000 – $6,000 = $24,000

- Net Yield: ($24,000 ÷ $400,000) x 100 = 6.0%

Condo B (Older Building)

- Annual Rent: $30,000

- Annual Expenses (higher taxes, insurance, hefty HOA, more repairs): $11,000

- Net Income: $30,000 – $11,000 = $19,000

- Net Yield: ($19,000 ÷ $400,000) x 100 = 4.75%

The difference is stark. Condo A is putting significantly more money in your pocket each year—a critical fact completely hidden by the gross yield calculation. This is precisely why knowing how to calculate rental yield with precision is essential for any serious investment analysis.

So, What’s a “Good” Rental Yield, Anyway?

You’ve crunched the numbers and have your net rental yield staring back at you. Now for the big question: Is that number actually any good? The truth is, there’s no magic percentage. A “good” rental yield is never a one-size-fits-all figure; it’s all about context.

What looks fantastic in one market might be a massive red flag in another. The ideal yield is shaped by your local market, the type of property you own, and, most importantly, your own investment goals. This is where understanding revenue management in rental properties becomes critical, as it’s all about tweaking pricing and occupancy to squeeze the most income out of your specific situation.

Cash Flow vs. Long-Term Growth

Your entire investment strategy dictates what a “good” yield looks like for you. Are you chasing immediate cash flow to supplement your monthly income, or are you playing the long game for appreciation and equity?

A 4% yield in a neighborhood with rapidly rising property values might be a much smarter long-term play than an 8% yield in a stagnant area. One strategy builds wealth through equity, while the other puts cash in your pocket every month. Neither is wrong—they just serve completely different purposes.

This is where you have to get real with yourself and align your expectations with your financial plan. If you want to dive deeper into different approaches, our guide on some popular real estate investment strategies breaks it down.

Knowing these nuances is everything. Rental yields also swing wildly between different countries and even neighboring cities, reflecting unique local market dynamics. For instance, you might see yields as high as 9.95% in an emerging market like South Africa, while a stable market like Germany averages around 3.74%. These numbers prove why knowing your specific market inside and out is non-negotiable.

Ultimately, a good yield is one that fits the bigger picture of your portfolio and helps you hit your personal financial targets.

Don’t Let These Common Mistakes Kill Your Returns

A great rental yield on paper can vanish into thin air once the realities of property ownership kick in. Honestly, knowing the formula is the easy part. The real skill that separates seasoned investors from landlords who are always struggling is spotting the hidden costs that sabotage your returns.

One of the biggest blunders I see is underestimating the true cost of owning a rental.

New investors often draft up a budget that conveniently leaves out all the annoying, less-obvious expenses. It’s never just the mortgage and taxes. It’s the slow, steady drip of a dozen other costs that quietly eats away at your profit margins month after month.

Stress-Test Your Numbers Against Reality

You absolutely have to build realistic financial buffers into your calculations. That’s non-negotiable if you want to protect your cash flow. A fantastic-looking yield can flip negative after one unexpected HVAC replacement or a single month of vacancy.

Here are the key areas where I see investors get their math wrong all the time:

- Underestimating Maintenance: Those charming older properties? They come with bigger repair bills. A solid rule of thumb is to budget 1-2% of the property’s total value every year just for maintenance. Don’t skip this.

- Forgetting Tenant Turnover Costs: Vacancy isn’t just about lost rent. It’s about the money you spend marketing the unit, screening new applicants, painting, and making small repairs between every single tenancy.

- Ignoring Local Laws: This one can be a killer. Landlord-tenant laws can dramatically affect your expenses and timelines, especially when it comes to things like evictions or property standards you’re legally required to meet. Always operate in compliance with Federal Fair Housing guidelines and local ordinances.

The most dangerous mistake you can make is assuming your initial calculations are set in stone. Your rental yield is a living number, and you have to constantly stress-test it against market shifts and those big, unexpected capital expenses.

Looking beyond your spreadsheet is just as critical. Broader economic trends matter. High construction costs can squeeze local markets, but some areas always seem to defy the odds. For example, cities like Caucaia in Brazil have shown rental yields around 7.2% even with wider uncertainty, which just proves how much local dynamics can influence your actual returns. You can see more insights on global real estate trends at JLL.com.

Of course, having the cash to cover these potential costs is everything. That’s why you should also check out our guide on how to finance an investment property.

Common Questions on Rental Yield

Even after you get the hang of the formulas, a few questions always seem to surface. Crunching the numbers is one thing; understanding what they really mean on the ground is what separates the pros from the amateurs. Here are the answers to the questions I hear most often.

Does Rental Yield Include Property Appreciation?

No, and this is probably the most important distinction to grasp. Rental yield is a laser-focused look at the cash flow your property generates against its cost. It completely ignores whether the property’s market value goes up or down. That’s appreciation (or capital gains), and it’s a totally different part of your return.

Your total return on investment is a mix of both rental yield and appreciation. I’ve seen properties with a modest yield turn into incredible long-term wealth builders because they were in high-growth areas. On the flip side, a property might have a killer yield but sit in a market where prices haven’t budged in a decade. You have to look at both pieces of the puzzle.

How Often Should I Recalculate My Rental Yield?

I recommend my clients run the numbers on their net rental yield at least once a year. Think of it as an annual financial health check for your investment. It’s the only way to track how your asset is actually performing, not just how you projected it would.

Over 12 months, a lot can change. Your numbers will almost certainly shift due to things like:

- Property taxes or insurance premiums inching up.

- Rent increases you’ve implemented.

- A major, unexpected repair that threw your maintenance budget out of whack.

An annual review keeps your finger on the pulse and ensures the yield you’re looking at reflects today’s reality.

Can I Use Rental Yield to Compare Different Property Types?

Absolutely. This is one of the best things about rental yield—it’s a great equalizer. It allows you to put a single-family home, a duplex, a small apartment building, and even a commercial space on the same playing field to compare their income-generating potential.

But a word of warning from experience: always, always use the net rental yield for these comparisons. The gross number will lie to you. Operating costs, vacancy rates, and management fees can vary wildly between a residential home and a commercial storefront. Gross yield hides all those critical differences.

Ready to turn your real estate goals into a reality in Los Angeles? The experts at ACME Real Estate are here to provide the local knowledge and data-driven insights you need to make informed decisions. Whether you’re buying your first investment or optimizing your portfolio, your journey starts here. Explore your options with us at https://www.acmexserhant.com.